Mellon on the Markets

I’m on an Emirates A380 over the island of Goa, en route to Dubai from Melbourne. For the past ten days, I’ve been on a whirlwind visit to Hong Kong, where I spoke at the Economist Longevity conference, and to Australia, where I discussed, inter alia, lithium and more Juvenescence.

In less than two weeks, it’s a round trip to Sydney for the Sohn Hearts & Minds Investment Leaders Conference, where yet another speech beckons. Yikes!

This excessive travel leads me to two comments: one, an apology to the editor for the tardiness of this month’s letter; and two, the observation that jet age travel hasn’t really changed much in the fifty years or so I’ve been on planes.

Sure, the modern aircraft are more fuel efficient, less noisy, and in business class there are things such as flat beds – oh, and loyalty points. There is also a lot more security, for obvious reasons, and TV screens on which we can watch unwatchable movies.

But fundamentally, planes don’t go any faster than the old 707s and Comets which once roamed the skies, although in considerably fewer numbers. Planes go further, and generally (the A380 aside) have two engines, not four, but they are still proceeding at under 600 mph or about 1,000 kph, well below the speed of sound.

The only jets which go faster are military, or the late-lamented Concorde, beloved of the glitterati of its era, as well as a useful – though ruinously expensive – tool for the transatlantic business community.

I have heard talk of new forms of propulsion, of mini Concordes on the drawing board and of lightning speed inner space travel, but nothing has yet happened to demonstrate to me that within my (Juvenescent!) lifespan there will be anything other than plodding jet service involving tedious travel and horrid jet lag.

Could one of our readers not do a piece on how travel could feasibly and reasonably cheaply be made faster? It could be breaking news, and a lot more interesting than Sir Michael Fallon’s “brush with destiny” or any of the other Sexminster revelations.

A pain in the neck

I must say, I am amazed that markets keep rising, albeit in a narrower and narrower range. This is especially so in the face of clearly tightening labour markets, rising (or about-to-rise) interest rates and a slew of unsavoury revelations about Trump’s campaign, the European political wildfires, and a whole host of other nasties.

I am also bound to eat a big dollop of humble pie in that the FANGs have continued to roar ahead despite my King Canute effort to hold them back. Earnings out of Facebook, Amazon and Alphabet have been exceptionally good, which doesn’t really surprise me, but what does astonish me is that the political and regulatory clouds hanging over such companies have had so little effect. In due course, these factors will prevail, but in the meantime, I am licking the wounds that come from being a roasted bear. Ah well.

Some stuff is going well, including the march of Japan. When I was interviewed by my old friend Bernie Lo on CNBC in Hong Kong, I said that I thought the Nikkei would rise to 25,000 by the end of this year. I meant to say that it would be there by the end of next year, but at the rate it is proceeding, it may well be that the magic mark will be attained by this December.

For more insight and analysis like this, CLICK HERE to read Master Investor Magazine for FREE.

Japanese retail investors, who I remember going nuts for stocks in the 1980s, are now a considerably less numerous bunch, and not nearly as gung-ho. Only 10% of the Japanese adult population owns stocks, compared to 36% in the US. Everyone is a saver in Japan – they have to be with the oldest population anywhere in the world – and government bonds yield zippo.

Will Nutting of Stifel, a very fine analyst, is now with me on Sony (TYO:6758). It’s a raging buy and along with Japanese ETFs and Nikkei or TOPIX futures, represents a great way of getting exposure to the only major market that has real momentum based on fundamentals. The average Japanese will soon be looking at the stock market as a viable place for investment, with a modest but rising yield on stocks, improving earnings and relatively cheap PE ratios. Corporate governance is hardly pristine (see the recent Kobe Steel scandal as an example), but it is undoubtedly improving.

If it’s not too late, and the horse hasn’t completely bolted all the way to Kyoto from Tokyo, I will be writing in greater detail in April of next year when I visit Japan. It remains my favourite place to have equity exposure, in the round.

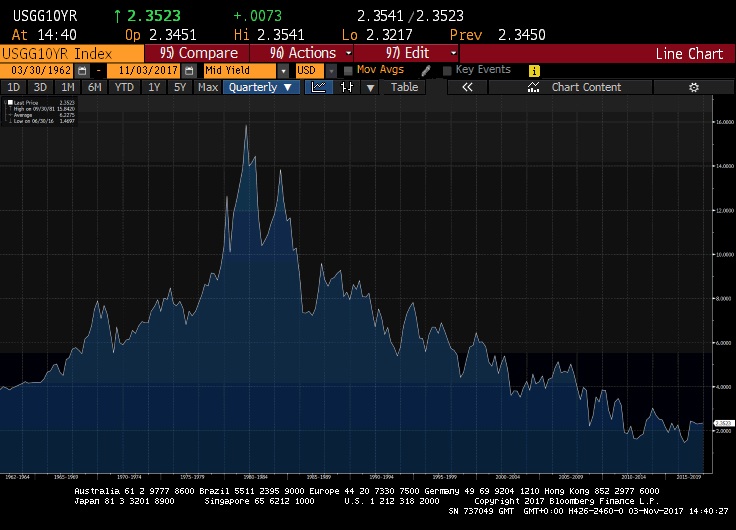

Approaching a “major inflection” for bonds and inflation

Elsewhere, bond yields sputter around but basically are not going down, and are showing the signs of a classic bottom, indicating the beginning of a bear market for fixed interest. Bill Blain of MINT thinks we might be at a major inflection point, and I agree with him. He’s normally right.

Everyone I know tells me the Philips curve is dead, and this week’s Economist says the same thing. I strongly disagree. I think inflation is both poorly measured and calculated too low. A pint of beer in an average Melbourne pub at A$14 tells you everything you need to know about inflation Down Under, as an example. And that’s after the currency has fallen 25% in recent years, from a peak of near parity with the US dollar.

The workers are revolting, and they are by hook or by crook going to get a bigger share of the pie. My own prescription for rectifying the inequality between corporate profits, which are too high and are generating huge piles of side-lined and useless cash, is to raise minimum wages in developed economies – and very substantially.

Forget about a Universal Basic Wage, which is a slacker’s charter and just another form of taxation; let’s try to avoid the destruction that would surely come from a Corbynite type government in the UK (and in many other countries) and just pay those on the lowest wages more.

Make it mandatory, and more people will work, people will be happier, economies will benefit from more consumer spending. But we will indeed get inflation, and more of it than everyone expects.

In fact, as the US economy grinds along at about a 3% growth rate and unemployment is at lower levels than for many decades, the inevitability of upward wage pressure strikes me as being obvious. In the 1970s, the developed world suffered a bout of massive inflation which has been largely forgotten – except by people like me.

For more insight and analysis like this, CLICK HERE to read Master Investor Magazine for FREE.

I am not suggesting that we are going back to double-digit inflation, but 3%, 4% or 5% is entirely possible. And remember, highly indebted governments love inflation as it inflates their debts away; central bankers like it too, since achieving inflation in recent years has been their overriding mantra. They are going to get it.

In those circumstances, all I can say is buy gold, silver – in fact any commodity that is in short supply and subject to inflationary pressures.

And on that subject, back to Melbourne. Backroom discussions with the best miners I know, and the best networker I know (my old friend Anthony Baillieu), tenements pegged and funding secured. Watch this space. Lithium will be a big focus next year.

One of our Master Investor 2016 tips, Critical Elements (CVE:CRE) is already up almost six times, and I have another tip in that area which will be revealed in a few weeks.

Happy Hunting!

Jim Mellon

Click HERE to follow Jim’s trades on twitter

Hi Jim, thanks for the great post as always. I’m an MBA student from England currently studying in the great state of Texas, and have been following the masterinvestor blog for about a year and a half now. Low wage growth is always an issue that bugs me.

A rise in productivity should, to some extent, give overall wages a boost. I believe I am correct in thinking low productivity has plagued developed economy for some years now. You can’t force employers to pay higher wages unless the state forces them to. I’m guessing your theory to improve wage growth is that non-skills jobs will see an increase in pay; therefore, companies offering skilled positions will be forced to pay higher wages too. I know this is alleged economics 101, but won’t this cut the demand for labour? or this inevitable due to other factors such as technology etc?

I have two suggestions to benefit wage growth; the first, to reduce subsidized pay and unemployment benefit, and two, set strict quotas employing foreign labour for low/semi skilled positions (post Brexit for the UK). This would, in essence, force employers to raise wages, or else nobody will want to work for them. Further, the unemployed will not be able to sustain a decent stand of living and will, of course, desire higher wages.

Do you reckon this is a feasible idea?

Cheers, Sam.

Goa is not an island but a state on the west coast of India, bordering Karnataka and Maharashtra less than an hours flight from Mumbai

Jim, what you are missing, why you make mistakes in FANG, bonds and others, is the unsayable…

What do the big banks, the Central Banks, big corporates and partially governments have in common…………?

(I’m 400% up… equities only)