It’s Game Over For Greece’s Creditors

“We found opposing us an axis of powers… led by the governments of Spain and Portugal which for obvious political reasons attempted to lead the entire negotiations to the brink.”

― Alexis Tsipras

An Unrealistic Expectation

During the last six years, global markets have been oiled by two major pipelines: at one side stands the global easing movement that enlarged central banks’ balance sheets as never seen before and helped financial assets recover and regain their previous strength; at the other side lies the perpetual negotiation between the bankrupt Greek state and its creditors, which has been driving a lot of enthusiasm among bond speculators and imparting some price dynamics to the Euro FX market. But the oil is drying very quickly as QE is not unlimited, nor is the ability of Greece to keep servicing its debts.

Much has been discussed over the course of the last six years, many measures were implemented to reduce debt, many sacrifices were taken by the Greek population, just to end, over and over again, at the exact same departure point. Greece may cut current and future spending but it cannot certainly cut past spending. While running a positive government budget balance from now on, some of the past excesses can eventually be paid for, but the ability to run budget surpluses is so limited that we usually refer to the government budget as a budget deficit. No matter how much effort is put into achieving a positive balance, Greece will never be able to repay a debt that amounts to more than 170% of its GDP. For that to happen, the government would have to surpass every sensible social frontier up to the point of confiscating from its citizens every cent produced during almost two years. But of course people would die before that. This way, the government can eventually confiscate, let’s say, 10% of what the citizens produce every year. In that case, and provided they were still able to produce the same every year, then the country would hit a level of 60% for its debt-to-GDP in 11 years time and eventually repay everything in 17 years. But for that to happen, the government would need to be able to confiscate 10% every year without leading the economy into a huge depression. The past serves as evidence to the contrary, as an attempt to confiscate much less has resulted in an annual GDP decrease of 4.9%. So, let’s now assume that pace continues. Being that the case, in 11 years time, debt-to-GDP would be reduced from 170% to 152%. To hit the healthy level of 60% (as specified by on the Eurozone rules), it would take more than 34 years. By then, the Greek economy would have contracted 80%.

But we can assume something more positive. Let’s say the economy grows 2% per year while the government achieves a surplus of 10%, a very unrealistic possibility. It would still take more than 9 years to hit the 60% debt-to-GDP mark.

While this example is simplified and extreme, I believe it very well depicts the current dilemma faced by the country. The more they cut spending, the worse GDP will perform and the more difficult it will be to reduce debt. So far we have seen that cutting government expenses is not paving the way for Greece to grow but rather sending it towards poverty. If I can see that, certainly the IMF can too. I don’t believe they ever thought Greece would repay its debts in full. They’re just buying time and are not really all that concerned about default this time round. However, in 2010, if no bailout were attempted, they would have lost a lot more due to financial contagion. But all this is not exactly in the best interests of Greece…

Realising the Truth

No government can expect to survive for long when there is no growth and unemployment is high. If I had to choose just a few statistics a government should concern itself with, these would certainly be at the top. Antoni Samaras ignored this, as he thought that by sticking together with creditors he could save the country. The problem is that he was not mandated by creditors and the interests of creditors were never aligned with the country’s interests. As a consequence the country was economically damaged and social unrest increased dramatically to the point the leftist party Syriza was elected and replaced Samaras.

Many European officials, as well as leaders of international institutions, have tried everything to scare the Greeks, always magnifying the negative consequences of changing government. They were successful at first but then after a few more years of economic contraction and high unemployment rates, the Greeks put an end to Samaras’ hegemony and mandated Alexis Tsipras to try a different path. For international creditors this could be a problem because it reduces the chances of being paid in full. But for the Greeks any change would have been a change for the better. As I mentioned above (even if through an extreme example), the odds of Greece repaying its debts are very slim indeed. The country should stick to a positive budget deficit but it will never achieve a positive enough number to reduce the debt stock in a significant way. This is the point at which game over appears on creditors’ screens and the losses should be recognised.

Someone Must Put a Stop to This

During the last few months, every kind of trick has been attempted to keep the Greek government in line with the past austerity programme. First we had the ECB trying to force Greece into a deal when they cut emergency funding; then we had the governments of other rotten countries undermining any kind of deal that would impose a marginal decrease on Greece’s sacrifice (as they eventually feared a contagion of a leftist wave to their home countries); and after that we had (and still have) the international creditors threatening to suspend the release of additional funds if Tsipras’ government doesn’t adopt austere measures. Tsipras was never intimidated and is unlikely to accept a deal that puts additional burdens on the country. Creditors want Greece to adopt more austerity to release €7.2 billion, just for the country to be able to repay €1.5 billion to the IMF in two weeks’ time. That’s absolutely insane. Greece is taking loans to repay other loans. When that happens, it is time to push the bankrupt button.

An Unfortunate Past

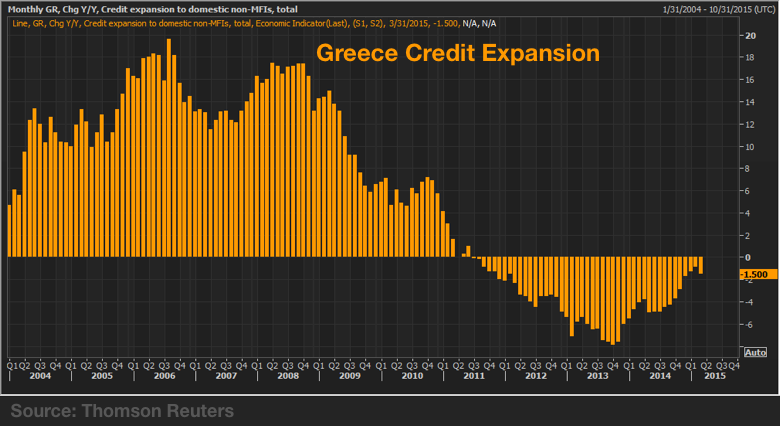

Over the course of many years, the Greek banking system (in part protected by the ECB) has been expanding credit. Credit expansion hit 20% YoY at times and was always very robust during the 2000s. It was only in 2010 that everyone realised that credit growth without accompanying GDP growth means that debt cannot be repaid. That is the point at which a loss should be recognised to those who lend.

But that didn’t happen. Instead of recognising losses, the Eurozone, the ECB, and the IMF preferred to lend to a bankrupt system. Not because they needed Greece to stay in the Euro but rather because lending more money to Greece would be cheaper than having to bailout the overly exposed French and German banks. In the end a collapse could happen, which would be dramatically costly. Bailing out Greece and extracting the most from them thereafter would be a much less costly route. A bailout was quickly arranged and Greece survived… for one year. The country received €110 billion in 2010 just to survive until a second bailout of €130 billion in 2011. A haircut of 53.5% on government bonds was also imposed by then as the bailout money wasn’t enough. A lot of money was released in the direction of Greece but at least most of the contagion risks were contained. However, the costs to Greece were very high. In less than two years the unemployment rate rose from near 10% to 25%.

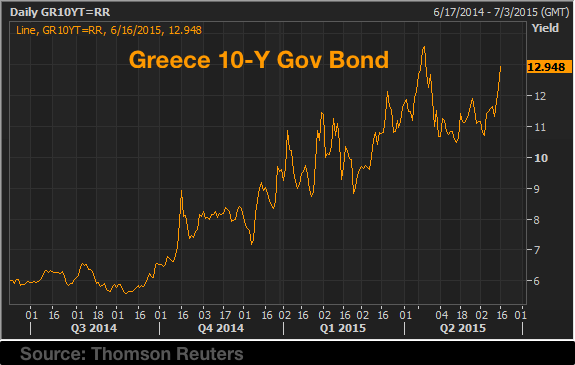

Unlike the promises of those who imposed austerity, there was never a recovery in employment levels. After hitting a record high near 28%, the unemployment rate just recovered a very pale 2.5% to the current 25.6%, which is a ridiculous and insignificant improvement. At the same time, the real GDP growth rate has been compounded at a negative annual pace of 4.9% for the last five years, as I already mentioned above. The bailout served the interests of some, but Greece isn’t among them. The current yield on a 10-year government bond is 12.95%, up from stable values near 6% in Q3 2014. Even though the yield doubled in less than 1-year it still seems ridiculously low for the current situation. Greece has no other option than to default. This game is over.

No contagion?

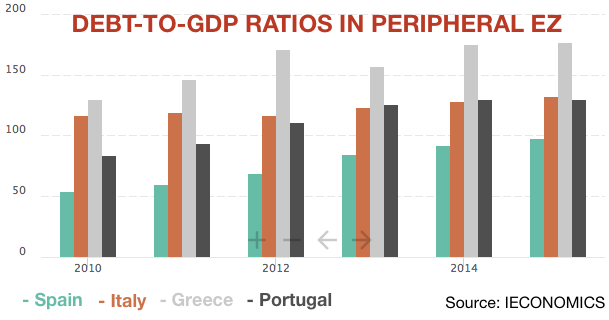

My final words are pointed in the direction of those who point the finger to Greece and those who believe everything will be ok, as they believe the damage is sustained. Despite what many think, a Grexit is not something to be taken lightly. The artificially low bond yields that have been supported thanks to the ECB intervention are now on the rise. In fact many yields are now higher than before QE started. Grexit means higher bond yields at a time the Eurozone economy is very weak. At the same time I expect the dispersion of bond spreads to increase to more realistic values if a Grexit occurs. What I mean is that countries like Spain, Portugal and Italy have been experiencing very low yields just because of intervention and not as the result of government reforms. Just look at the following chart. Can you identify any improvement?

If Greece leaves the Euro, then investors will understand that the fixed exchange rates between the 19 Eurozone countries are not irrevocably fixed, and that allows for huge speculation.

Regarding those countries that contributed most towards a failure of the negotiations, it is interesting to note that they will be the most negatively impacted by such failure too. That would open the path for new Syriza-like governments to succeed in those countries as well. I can see the smoke already…

Comments (0)