Is Portugal the New Greece?

Investors seem anxious, as they explore the implications stemming from the possibility of Portugal becoming another Greece. The general election culminated with the largest number of parliament seats being won by the centre-right coalition already in power, but still short of securing a majority. An emerging alternative coalition is on the cards, which may bring Portugal Syriza-like disruptions, investors fear. But one needs to ask if such a fear is really well grounded. Will a leftist coalition lead to a change in direction and to a disruption in financial markets? That is very unlikely! More than anything, Portugal is one of the best places for an investor to put their money in, and a change in government will not change that.

Portugal is at a historic junction where there is a high likelihood of its centre-left Socialist party (PS) making a deal with the Left Bloc (BE), which is often seen as a forerunner of Greece’s Syriza, and the Communist party (PCP-PEV), which has always criticised the current austerity and pressed for a renegotiation of debt. Such a deal has been widely repudiated by the current PM – Passos Coelho – who warned the Portuguese electorate on how their efforts could be undermined by such a deal and how the financial situation of the country could quickly deteriorate.

The Portuguese equity and debt markets seem to have aligned with the PM’s view, as they have been experiencing some increased turbulence as of late. The main equity index PSI20 has declined by over 4% so far this week, and the 10-year government bond yield has increased from 2.29% to 2.46%. The decline in the price of financial assets reflects the uncertainty regarding the next four years. Investors fear a push for debt renegotiations and the resulting fiscal indiscipline, if a leftist alliance arises.

Portugal is no Greece, as the PM has often said. While economic conditions are still very weak in Portugal, they are the worst ever felt in Greece, as the country is living its own Great Depression. The leftist parties in Portugal all learned from the latest developments in Greece, which served as a caution for all those pushing for debt renegotiations in Brussels. The EU made it clear that there is not much room for exceptions to its rules. Staying in the euro requires a strong commitment to European pacts. Any change in policy at the country-level can only be qualitative rather than quantitative, for all those willing to stay within the Eurozone borders.

Both the Left Bloc and the Communist parties showed their willingness to abandon any radical plans to renegotiate debt and increase the government budget deficit, in order to back a Socialist-led government. They learned from Greece that leaving the euro is not currently an option for the country and that there isn’t much margin for negotiations leading to exceptions. The euro is not at stake if a new leftist government arises, as the adopted policy direction will be in line with the prior coalition government of the past four years, in particular concerning the honouring of European-level commitments regarding debt reduction. The main pillars would remain intact.

As an alternative, we can still see the same centre-right coalition leading the country as a minority government. If that happens, they will struggle to find the needed support from the left, unless they make strong concessions. Again, the policy would qualitatively change but not quantitatively, as the main points will never be at stake. But while markets see the centre-right option as being the best, such an outcome may in fact result in more instability. The minority achieved by the centre-right requires too much negotiation with the Socialist party, which will lead to intense struggles that may never be overcome. If that were the case, a new general election would be necessary, but that could only happen in six months’ time (because of Portuguese legislation not allowing for a quicker dissolution of Parliament). The first tough hurdle to overcome will be the discussion and approval of the government budget for 2016, scheduled in just a few weeks’ time.

A minority government without strong support from the Socialists will bring volatility to the equity and bond markets for the next six months.

A Pyrrhic victory

Unlike what happened in 2011, when the centre-left coalition won 132 of the 230 seats in Parliament, the coalition now only holds 107 seats, a number that falls short of the 116 needed for a majority. With the leftist parties holding all other seats, it is technically impossible to form a stable coalition led by the centre-right. Passos Coelho, the Portuguese PM, won’t be able to command the country in the same way he did in the past. Policy will become more left-oriented. The change will eventually lead to increased volatility in markets but not on a scale many expect. The country continues to be supported by the ECB, as far as it sticks to its creditors’ plan, which caps any increase in debt yields.

As I mentioned above, one shouldn’t expect much change from either government configuration. Apart from further potential for volatility, the good prospects for the Portuguese equity market remain in place. According to StarCapital research, Portuguese equities are among the most undervalued in Europe, with the CAPE (cyclically adjusted price earnings) index hovering around 10.4x (according to data collected at the end of August). This value compares with 12.7x in the UK, 17.6x in Germany, 26.6x in Ireland, and 24.1x in the US. There is value in the Portuguese market and any price decline due to election uncertainty will just unlock extra profit potential (because there won’t be a break with the past in either political configuration).

Regarding the debt market, the yields on Portuguese government bonds are already on the rise. A 10-year bond is now yielding 17 basis points more than before the elections, but the upside is capped by central bank intervention. As long as Portugal honours its commitments to creditors, the central bank will continue to support the country. If yields rise during the next couple of weeks or months due to uncertainty, they will end up reverting, as greedy investors will by then start replacing other low-yielding Eurozone debt with Portuguese debt. That was not the case in Greece because the country was at the verge of leaving the euro and defaulting on debt obligations. Such an outcome is very unlikely in Portugal.

The Past in Numbers

During the last few years we have listened to European policymakers talk about the necessity of implementing austere measures in order to repair government finances, while also warning about the negative impact any alternative could have in the economy. While there is a strong and widespread agreement regarding the need to reduce government debt, there is also a recognition that the plan has failed. Portugal is no exception.

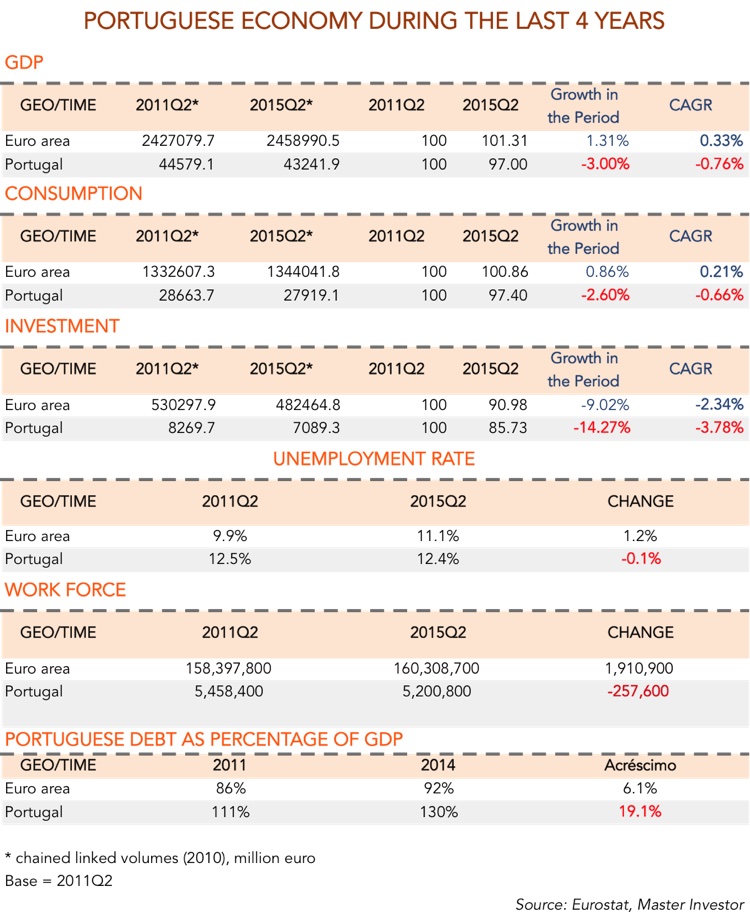

During the last four years, the coalition government has strongly committed to its creditors’ requests to implement austere measures to bring down government debt. Many budget cuts had to be made and, as a result, the country entered a dormant state, unable to recover from the past crisis. Real GDP is now 3% lower than it was four years ago, as is consumption. The adopted measures reduced the disposable income of households and led investment to retreat by more than 14% in the same period. This observation corroborates my thesis that there is no investment if there is no aggregate demand. Policies aimed at improving business conditions, by cutting corporate costs, just lead to higher profits that are never reinvested. That is particularly true when aggregate demand in very weak. Faced with such weak demand, companies prefer to repurchase shares, pay higher dividends and replace equity with debt instead of accumulating capital in the production. The coalition placed too much of the burden of budget cuts on the consumer, which contributed to the aforementioned outcome.

Despite the weak economic performance, there was a decline in the unemployment rate from 12.5% to 12.4% in the four year period. While this is a negligible decrease, it sounds odd. We know that for the unemployment rate to remain unchanged, the economy needs to grow by at least 2% per year. How could the unemployment rate remain unchanged under the current economic conditions? The key to the apparent puzzle is in the decline of the work force. Strong legislation changes mixed with weak economic conditions pushed many to leave the country or to just give up seeking a job. In just four years, the workforce declined by 4.7%, as 257,000 left. This explains why the unemployment rate hasn’t risen. If we add 200,000 back to the workforce as unemployed, the new number for the unemployment rate would then be 15.5%, which seems much more realistic.

While the economy contracted, the government was still unable to reduce the country’s debt position. Debt represented 111% of GDP in 2011 and has since risen to 130%.

The Future

For a small economy like Portugal, there’s not much that can be done in terms of fiscal policy to boost growth, as European rules limit the scope of action. Quantitatively the numbers won’t change with a government change, as EU requirements will continue to impose the same limits as before. But, the new government may focus more on households and disposable income, which would help aggregate demand to recover and finally push companies to reinvest their profits. More than seven years after the peak of the crisis, it is worth trying a slightly different approach.

Comments (0)