Desperate Measures in China

The Chinese saga is only getting started, as the country surprises the markets with ever more desperate measures. After spending almost $150 billion trying to contain a stock market collapse and declaring short selling as “malicious”, China is now devaluing its currency by the most in 20 years, as exports dropped 8.3% in July. While no one can mention recession – China is still growing much faster than any developed country could ever dream – the mismatch between the stock market and the real economy is increasingly evident.

A wave of positive sentiment helped equity prices in the past, contributing towards a disconnect from intrinsic values, but it seems sentiment is now reversing, as investors are pulling their money out of the market. At a time when economic conditions have been deteriorating in China, it could only be with awe (disbelief?) that one digests the one-year 80% rise in A-shares. The Chinese have been attracting naive investors to the stock market to help fuel the rally, but this attempt to keep prices inflated at any cost is just contributing to an ever bigger bubble. The big question is not whether there is a bubble or not, but whether the Chinese authorities can perpetuate it or not. In my view, they can’t.

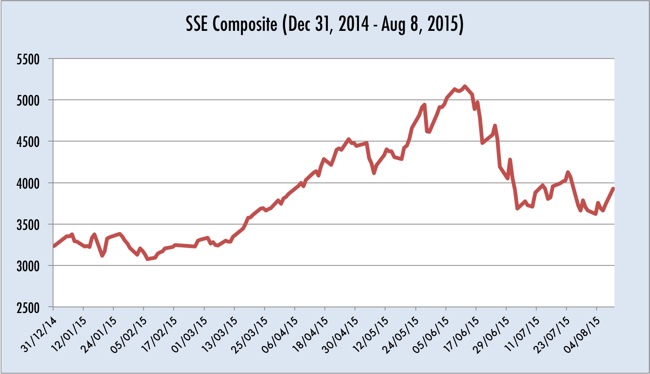

The SSE Composite is up a healthy 21.45% on the year. A-shares, as tracked by the FTSE China A-Shares All-Share Index, are up an even healthier 32.16%. In a one-year window, the rise in the same indexes has been 21.45% and 79.47% respectively, denoting a strong bullish momentum.

But while the above data shows a strong performance from Chinese equities, it hides an inconvenient truth: the market is becoming riskier, more volatile, and prone to a crash. The SSE Composite has experienced a very wild ride between June and July and in less than one month it lost 32% of its value. While the current year-to-date performance is strongly positive, the market is one quarter off highs.

The SSE Composite recorded declines north of 6% in five sessions this year. The increase in volatility has been notorious, but a crash hasn’t taken place because the Chinese authorities have prevented it. To stem the decline, authorities have been chasing short sellers and imposing several restrictions to make it harder to sell shares. But when short selling is limited, the market loses one of its most important adjustment mechanisms that helps prices converge towards equilibrium. At times when there is a disconnect between prices and fundamentals, short-selling is the only mechanism that helps prices return back to earth. Markets where there are significant short-selling limitations are usually more inefficient and prone to bubbles. But, I guess that what the Chinese authorities want is not an efficient market but rather an ever-rising one.

The cracks are now evident, as the government is becoming desperate. Spending around $144 billion to keep prices inflated and devaluing the currency against the dollar by 1.9% are desperate measures that are taken at desperate times.

With the US Federal Reserve now preparing to start a new interest rate cycle, companies will have to rely on themselves to grow. Stock prices will suffer because they have been propelled higher artificially and the deterioration in sentiment will spread round the world. Emerging markets, where sentiment is a key driver of stock prices, are more exposed to a shift in sentiment. It will be ever more difficult for the Chinese authorities to keep the market at these levels… unless they can set a scheme where only the coalition of state-owned financial institutions – the “national team” – is allowed to trade shares.

Comments (0)