Three Recovering Goldies

A key milestone mining investors look for is the ‘first pour’ of gold from a new mine. In theory that is when rewards start to be earned for the years of calls on them for more and more cash to build. And if the new is promised within a year to double production from an existing mine, you would think investors would be looking hard.

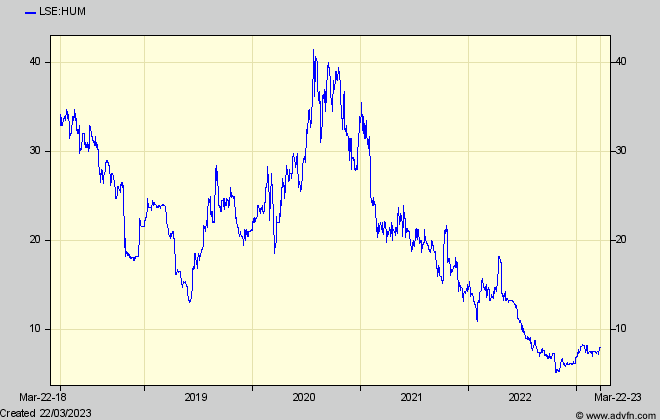

If, in addition, its owner had just attracted a large local investor to inject around 27% of new equity into its shares, you’d have doubly thought so. Hummingbird Resources (HUM) – market cap a mere £45m in relation to a promised 200,000 oz annual gold production worth some 7 times that – is in such a situation, but its shares haven’t exactly sparkled – except perhaps up to now. I said last time I would check.

Lack of sparkle is due to a rocky recent history and resulting investor scepticism. Back in 2018 (see MI Feb 2018) HUM was riding high with its relatively new, high grade Yanfolila gold mine in Mali in full production. But savvy investors and earlier backers were about to pull out of the shares, because, while its broker was touting their ‘value’ (based on an NPV for a gold resource that they didn’t mention was actually running out) the savvy knew that much money was going to be needed to extend Yanfolila’s life. In the event over $100m had to be spent to do just that, but was rewarded with substantially growing profits (and a recovering share price) up to 2020, only to be hit in 2021 by production difficulties and covid which cut Yanfolila’s production by 16% with higher costs, so that cash profit collapsed to 1/3rd that in 2020.

That poor performance continued into the 2022 1st quarter but, after a brief improvement in the 2nd, once again the third quarter suffered from what HUM reported was the poor operational and management performance of its mining contractor, who it has since stepped in to help improve. The result was that borrowings including a further loan for Kouroussa had reached $85m at end September.

Since then in early February, HUM has reported a strongly improved result, with Yanfolila producing a record 28,264 gold ounces in its last quarter – 67% higher than in the previous one, although net borrowings (including spending on Kouroussa which in September had committed 80% of its budget) had reached over $110m.

And a day later the company reported that African investment co CIG SA had agreed to inject $15m into HUM by way of 157.1m new shares at 7.8p – giving it 27% of the equity. Subsequently an open offer to shareholders at the same price has resulted in another £3.6m being raised, and shares in issue now over 622m (including management options) and a potential £47m market cap (compared with £140m at the last 2020 peak) – against net borrowings of possibly $120m by mid year.

So the question now, assuming Kouroussa performs and Yanfolila maintains output, so that group annual gold output reaches over 200,000 ounces (say by 2024) at the costs estimated for the former, is the current share price excessive or a bargain ? At $1,900/oz, and the less than $1,500/oz costs forecast ,Yanfolila would deliver at least a $34m annual gross profit, while Kouroussa’s feasibility study showed average free cash over an initial seven year life of $45m per annum. That would enable rapid repayment for the Kouroussa loans – just as HUM has successfully done for Yanfolila.

On top of that, I haven’t mentioned HUM’s third, yet to be built project, Dugbe in Liberia – twice the size of Yanfolila and Kouroussa combined. It has 2.76Moz gold in Reserves and strong economics showing a 3.5-year capex payback period, a 14-year life, and low costs (at 2021) of US$1,005/oz.

But lacking funds to develop itself, HUM has partnered with Canada’s TSX-V listed Pasofino Gold who has earned 49% of Dugbe by producing a feasibility study and has indicated it wants to acquire the remaining 51% in exchange for Pasofino shares. Those shares could give HUM financial flexibility which would allay whatever risk investors might continue to see on its own. A risk that will be further diminished if gold continues strong.

So all in all, with a hopefully small chance that delays over the coming months might hold the shares back, HUM looks to me a good speculation.

The company agrees. ”With the operational performance improving at Yanfolila, and Kouroussa on track to commence production by the end of Q2 2023, the Company is at a pivotal juncture for significant growth, with expectations for improved cash flow generation, a stronger balance sheet and a solid platform for further growth in H2 2023 and beyond.” But some investors, bitten by Yanfolila’s rocky last 18 months, might need persuading.

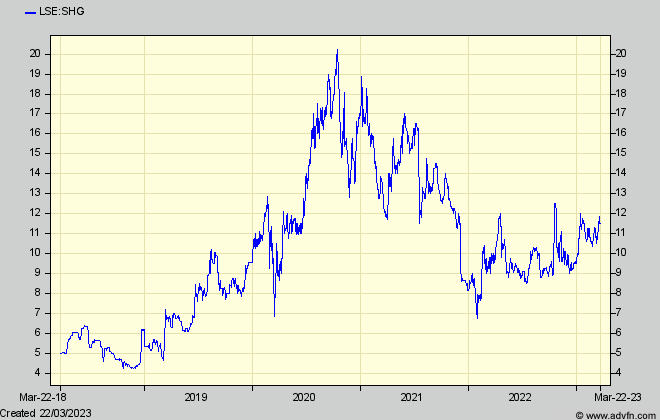

Shanta Gold (SHG) – on the other side of Africa in Tanzania – is similar to HUM in many ways. It has a producing mine, another due to start operating this year, and a third being explored which promises to be bigger than the other two. It also had production difficulties in 2021 which slashed output and its share price. Its gold output is smaller and so is its balance sheet with much less borrowings. But of course it is just as much exposed to the gold price. And its market cap ? – Three times bigger than HUM! Next time I’ll examine why, and whether that might continue.

Now for Atlantic Lithium (ALL) who I’ve always said is (always) just a little too expensive, despite eyewatering broker forecasts. Its shares have collapsed due to a notorious US short seller attacking ALL’s biggest customer’s shares, on the grounds that ALL’s Ghana lithium mines are in hock to some sort of African political skulduggery (all denied by ALL). So investors might wonder if this is a buying opportunity. But I would still say no. The lithium price weakness could last for some time, and the Ghana mine doesn’t start producing for at least another two years during when a lot could happen. A good rule is that large, promising looking, project shares like ALL’s, often spurt at the early stages when brokers tout the expected high profits without mentioning the high development costs, following when they tend to take a rest for a few years while the financial details, and the likely costs to investors, become clearer.

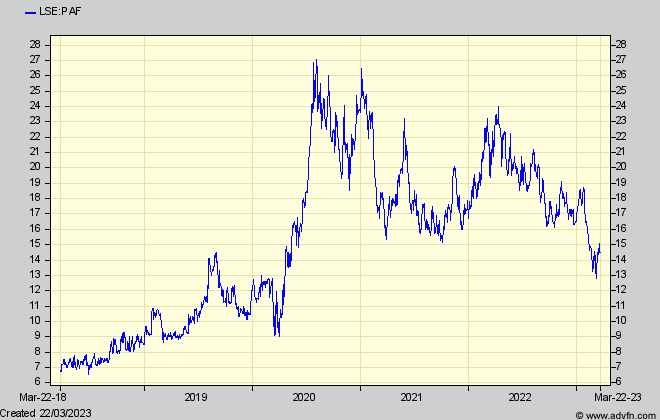

I’m conscious that I need to explain Pan African Resources’ (PAF) abysmal recent share performance, having flagged it last time as one of the few reliable goldies. More next time, but at base it is due to continuing labour unrest at its largest mine which was not disclosed to the market at the time, and the consequent share weakness impeding the need to raise funds to close the remaining, small, gap in funding for the ‘promised to be highly profitable and to add significantly to production’ Mintails project. That gap has now been filled with an eye-wateringly expensive but thankfully small streaming deal, which in my view, and seemingly of most others, is now water well under the bridge, leaving PAF at a historically and undeserved low rating. I think the shares should certainly be held for a substantial recovery in the medium term (and pending my more detailed update next time).

Comments (0)