Mining Doldrums

They seem to go on and on (as they do). Small explorers especially are drifting, submerged along with commodities and, until now, gold – still 5% off its US$ peaks against all the rumours of a new BRIC gold-backed currency – which the market obviously doesn’t believe.

Galantas Gold (GAL) and Wishbone (WSBN) are among the drifters, despite activity on (and under) the ground which will bear some sort of fruit eventually. However Galantas, while having just reported very significant gold and copper intercepts at its Scotland Gairloch project, has also clocked up a dire looking balance sheet which doesn’t bode too well for current shareholders – including me.

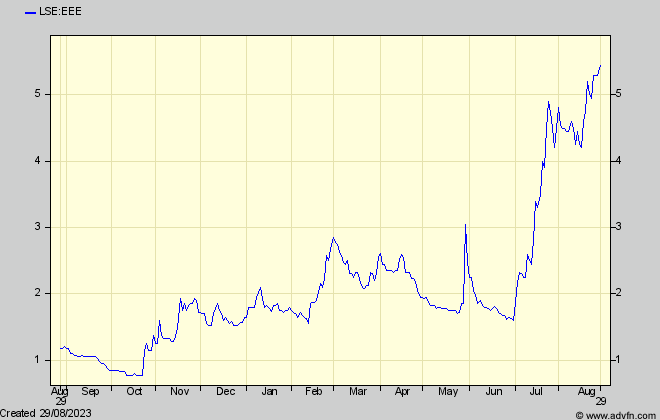

Meanwhile a new Aussie exploration darling in the form of Empire Metals (AIM:EEE) has surfaced reckoning it has stumbled upon one of the world’s largest copper and titanium deposits. It all remains to be seen from further drilling but, meanwhile, mining punters might have a field day. I’ve bought a few to see what happens next.

Unlike Xtract Resources (AIM:XTR) – one of my few turkeys, having turned out to have one of Mark Twain’s holes in the ground, in Australia, with a liar on top. Its got an income from its small African mines however, whose amount hasn’t yet been accurately established, which might help towards CEO Colin Bird’s latest wheeze – a copper exploration joint venture (“in a highly prospective part of Northwest Zambia where competition for exploration licences is acute.”) where Xtract will earn a 65% interest through exploration spending over an initial two-year period, of not less than US$2 million. Lets hope the income will cover those costs without a fund raise. I can’t see the shares doing anything but drift even lower meanwhile.

Even Barton Gold (ASX:BGD) is marking time, despite doing well to have found yet more gold down the back of its gold treatment mill to add a potential US$2.6m cash – (I use US$ instead of Aussies to avoid investor confusion) to the US$3.1m it has just raised from new and existing shareholders to start promising re-exploration soon of its historic licenses. It certainly merits holding as an explorer who might spark into more life earlier than some.

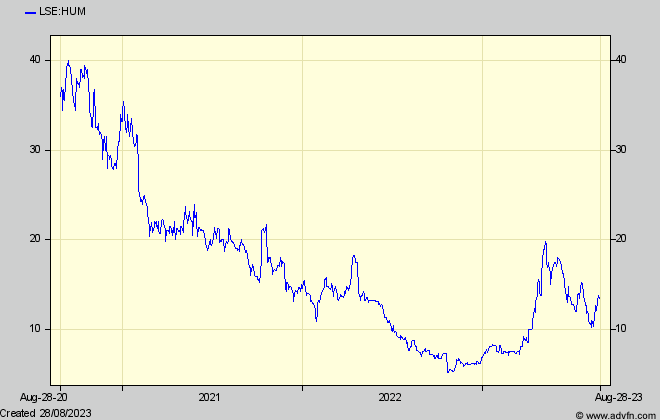

That means the only thing remaining to discuss is news on the few miners approaching start of production. Hummingbird Resources (LSE:HUM) to start with.

I did say ‘don’t sell’ in my June update. But I didn’t see those doldrums continuing which is the only reason I can think that caused HUM’s shares to sink back 30% to just over 10p after publication of its operational update three weeks ago for the quarter to June.

The pessimists were able to walk the shares down at first despite there being no just cause that I can see. They latched on to the lack (yet) of any paydown of the debt built up over the last few years as a result of the poor results at the existing Yanfolila mine last year and the start of building its second producing mine at Koroussa this.

But I wouldn’t have expected any paydown yet. Kourossa only achieved (on time) its first gold pour a few weeks ago, while capital spending hasn’t quite stopped and, as I said in my June update “projecting this year’s results in any detail in such turn-around cases is impossible, because in addition to Yanfolila swinging back into a decent profit but at an unpredictable rate, will be Kouroussa’s contribution (swinging from consuming cash to build, to building cash – also at an unpredictable rate)”

So the optimists have pushed the shares somewhat back up, only to encounter rumours of war between Niger, and the West African States where Hum operates – although well away from the borders where conflict might arise.

HUM itself is optimistic, expecting debt payback from Kourousa to start in this second half, although it also expects costs to rise temporarily at Yanfolila while it switches from mining one pit to another. Maybe that, and the uncertainty, still, of what Kourousa’s ramp-up costs will be is another plank for the pessimists, but I would have thought the scope for initial revenues from Kourossa is now so large, that it will outweigh any further – probably minor – problems elsewhere. Hummingbird is expecting Kouroussa to ramp up from zero to having produced 30,000 gold ounces by the year end, compared with 51,150 ounces from Yanfolila in this year’s first half. The company isn’t yet guiding for Kouroussa’s costs, but will do so in its October operational update. Meanwhile, I suggest don’t sell even though the shares might drift for a bit.

And now for a bigger theme – Mining Industry Costs.

Horizonte Minerals (LSE:HZM) – which is my other miner on its way to production with, hopefully, the end of the tunnel for shareholders – has flagged the problem. (Although I also have in mind Greatland Gold’s 30% share in Newmont’s Havieron gold mine now building its mine access, where I fear investors are in for a shock when the updated feasibility study is published (late) early next year. There are many others).

To recap why I follow HZM. It is one of this decade’s few stand-alone miners (ie directly accessible to investors, unlike many developing mines hidden inside big groups) progressing to be a major supplier of one of the most in-demand metals – nickel. Once in production it promises to be highly profitable and, after many shocks for them, profitable for shareholders.

But when?

Appearing to be successfully on track to first production early next year at the first stage of its Araguaia Brazilian nickel project in a presentation only two weeks before, HXM shocked on Aug 17 by warning of a risk that cost increases in the remaining part of its $532m construction budget (62% spent so far) “linked to several of the major construction packages including labour, materials and productivity, could result in future drawdowns on the senior debt facility not being permitted and require the Group to pursue alternative sources of funding to meet its commitments.”

But it also said “The Group has cash reserves and access to liquidity which are considered sufficient by the Directors to fund the Group’s committed expenditure both operationally and on its exploration project for the foreseeable future”.

I don’t know what that means. Was the warning just prudence?

Having navigated through numbers of shocks – I and all others had probably thought the end of HZM shareholders’ pain was in sight. But I did point out in Nov 2021 the sheer complexity of the funding package that had been agreed, and urged caution until, a year later in December 2022 I asked “Are we there yet” and then, last February said “Although I suggested the share chart was saying not to chase, their surge from 90p to 140p at the New Year, occasioned by the prospect of production starting later in2023, is showing signs of breaking out up to over 150p” But I went on to say .”Although HZM looks cheap on that production prospect, sooner or later the market will worry about the large share dilution coming along as warrants, options, and streaming revenues, raised to get production going, start to be paid. But no doubt investors will ignore that for some time yet.”

They did, pushing the shares above 160p after a US institution bought 5% only a few weeks ago.

But that was before the latest warning, and now we are back in no-man’s land, with many investors buying in advance of the August half-year update probably hopping mad. Not that many more than normal appear to be selling, even though the nickel price has come back (along with every other commodity) a long way from its $30,000/tonne top earlier this year.

Its not the first time warnings about cost increases have dogged HZM’s shares. The reluctance of institutions to put up funds at the 10p that was being bandied about a few years ago came about after what I had described as ‘the 46% ‘staggering increase in capital cost’.

To recap from my list of possible downward pressure on HZM’s shares that I estimated nearly two years ago. Interest, loan repayments, streaming, and royalties, on the original basic funding package will be c $75m annually for 9 years. In addition, the company said (then) the $251m cost of stage two will be financed by stage one’s cash flow. Stage three (a new project, at Vermelho) will cost in the same region as one and two together, and as well as using up early cash flow will probably need more loans and more share issues. Those figures compare with the $180m annual cash income I tentatively estimate from stage one at a $23,000/tonne nickel price. (now $21,000)

Those figures are now out of date. Share dilution in the pipeline from stage one funding will further reduce cash income per share. Instead of loan repayments there could be conversion into more shares in addition to those outstanding for options. The then 269m shares in issue (compared with 190m a year before and 85m just before that) hasn’t changed much in the last year, but my estimate even last year was they could balloon to 325 million, much higher than the optimists ever feared.

So it looks as though I have to repeat what I said a year ago “I see the coming year while stage one construction completes and first revenues come into view as a tussle between the nickel price, and investor fears of the cash outflows to fund stage two and to repay those funding sources.”

And also as before ” It means I wouldn’t chase the shares just yet unless they drift back a lot.” (from 140p).

The ‘market’ wants to see measurable success in the form of monetisation, and dare I say it, dividends. Those juniors that can bring regular monetisaton to an asset that is clear to understand, while holding out the prospect of a distribution will be the ones in demand. Over 90% of AIM Juniors have not got a chance of delivering £ any time soon, so it’s a matter of when they tap the market for cash, not if. Some juniors hold out the possibility, but not the certainty, of several monetisable assets that could provide regular income, whilst having several other assets that are ripe for JV or sale. Eventually capital will find its way to those Juniors and I reckon it will be in large volumes of £.

Jam today is required.