Metminco – Getting out of Its Bind

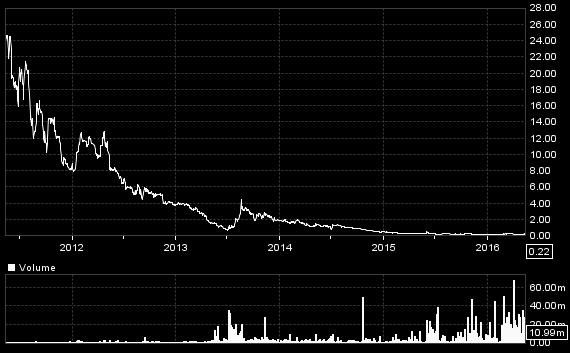

Practically all miners saw their shares decimated between 2011 and 2015. Avocet, whom I covered last week, was an extreme example. To look at Metminco‘s (MNC) chart with its shares now at 0.25p against 25p in 2011 might suggest the same. But where I think Avocet is a dead duck (an avocet, unfortunately for my freedom to choose a good headline, doesn’t look anything like a duck), at least in its present form, Metminco is better described as a dozy duck, although it would even better be thought of as a Phoenix in waiting. Unlike Avocet, which wasn’t able to get any shares away at all, Metminco’s shares in issue have quadrupled since it listed in 2010, so its loss of market value isn’t nearly as bad.

MNC – 5 yrs to May ’16

You could say that while many shareholders on miners’ bulletin boards castigate their managements for their loss of value, the reality is that most have been the victims of bad luck overtaking previous optimism. (I don’t think one should ever accuse entrepreneurs of ‘over-optimism’. The world would stop without them.) When MNC started up in 2005 looking for exploration prospects in South America, copper was in the middle of a surge from around $1/lb in the preceding ’90s, to reach over $4/lb in 2010, when Metminco became public at 10p per share. That was at the tail end of the ‘commodities boom’ engendered by long years of under-investment in new mines, and prices surging in anticipation of continuing under-supply.

The trouble is that finding new mines and bringing them to production always was going to take MNC some time. So now that after ten years it has indeed found almost exceptionally good, potential mines and has almost readied them for production, it has fallen foul of the copper price slump bind where it has become stuck. And one more piece of bad luck, though probably not as serious, has also come to hang over it.

If it weren’t for copper slumping to hardly more than $2.1/lb now against $3/lb only two years ago, MNC’s hard work would have been rewarded with two potential mines which it has developed to where their economics promise to be at the higher end of world copper producers. Its flagship (if it is the correct term for something still in dry dock) is the world class Los Calatos deposit in Peru, whose economics according to a 2014 study showed over £30bn worth of in-ground copper (at $3/lb) and a more than 30 year mine life at a lower than industry mean cost of only $1.1/lb – but at a capital cost of $1.3bn

In contrast MNC’s market cap now is only £8m, despite its Aussie mining specialist broker saying “Los Calatos is one of the few, substantial, copper – molybdenum porphyry projects that has been advanced to a Pre-Feasibility Stage, and is wholly owned by a junior exploration and development company.”

If that $1.3bn capex has proved to be too much for a minnow like MNC, it also owns the much smaller but even more profitable Mollacas project in Chile, where a 2014 scoping study showed that for a much lower $47m capital cost it could earn a 37% IRR and a $75m NPV8 on a 7-year mine life – although still at the then $3.1/lb copper price. But unfortunately, if a copper price that is now 1/3rd lower wasn’t enough to render Mollacas (for the moment) almost uneconomic, a landowner has been challenging MNC’s access to (but not ownership of) the mine and has thereby forced its development to be put on hold while MNC negotiates, having taken its case as far as it can in the Courts, and losing.

So, while the Mollacas landowner will, surely, be brought round at a cost, it is the copper price that has effectively stopped MNC’s engines. Before copper’s latest lurch downwards, in an effort to reduce the daunting capex for Los Calatos, MNC reworked its mining plan to concentrate on higher grade portions of the original pit design (and to go, more cheaply, underground) so as to halve that $1.3bn capex and in the process achieve a still excellent 16.6% IRR and a $447m 8% NPV. (Although, again, at a $3/lb copper price.)

In the present, probably temporarily much worse environment for copper, that capex, also, is too daunting a prospect for MNC to fund, so it is detailed negotiations with a number of larger potential partners to help pay for the further work necessary before Los Calatos can be developed on that smaller scale, which even if involving giving most of it away, might at least release some nearer term value for shareholders. Given the mine could potentially commence in late 2020, such partners might hope to see Los Calatos coming into production at a time when industry expectations are for a shortfall in global copper supplies and therefore a higher price. On top of that, Los Calatos has good further exploration opportunities that will add to its attractions.

But even if that isn’t enough, MNC is on the verge of a deal to counter any prolonged copper weakness by diversifying into gold – where there is a plausible case to say that if copper remains weak it will be because the global economy stays weak, engendering desperate stimulatory measures which will increase indebtedness and so stimulate the price of gold. So it makes sense for MNC to be hedging its bets between the two metals.

Its agreed deal to pay an initial A$2m (approx £1m) in shares (and, later, up to $7.5m in cash if it decides to mine) to buy the Quinchia portfolio of gold assets in Columbia should be complete by the end of May. Quinchia comprises a late-stage 1.8Moz gold mine at Miraflores, not far from Anglo-Gold Ashanti’s giant 33Moz La Colosa gold mine and others on the same structural trend, and has a number of other deposits and prospects which, so far, total 2.8Moz of gold resource.

Miraflores is being acquired on the cheap, after its owner went bust just before completing a feasibility study and after spending $29m. From there a subsequent owner commissioned a more detailed technical report on a mining plan providing for a 12-year mine life recovering an average 42,000 oz of gold per annum at a $682/oz cash and sustaining cost, in return for an initial $83m capex – an amount that currently is more easily funded for gold than for copper. Once the deal completes, taking its shares in issue up from 3.4bn to nearly 4bn, MNC plans to complete the feasibility study, which hopefully will optimise the mine to lower costs and increase production by 30% to 55,000 oz/year, so bringing more cash flow earlier. This will all take more funding of course, but if the gold environment continues to improve there should be no obstacles to MNC raising what it takes to get Miraflores into production and deliver the cash flow it needs to develop its other projects.

Of these, Los Calatos has by far the greatest scope with its opportunities for longer term expansion, which are what will attract a funding partner, so that MNC’s challenge will be to keep its various plates spinning in the air, with the Mollacas project as a wild card. The latter is the best prospect to deliver near-term cash flow, and it seems unlikely that the landowner blocking access would spite his nose so severely as to refuse to compromise and allow it to proceed.

MNC – 1 year to May ’16

MNC’s shares don’t seem to have reacted much to the Miraflores key to releasing it from its bind – perhaps because there has for long been a perception that its projects having stalled and its share dilution (not as bad as for many other miners) is all MNC’s management’s fault, but also perhaps because recent share placings and options conversions to keep going have released shares onto the market. And further fund raises to keep the plates spinning are obviously on the cards.

MNC’s primary listing is on ASX, whose investors are possibly better mining judges than us Brits, so will determine the shares’ medium term performance. The AGM is due next week in Sydney and might deliver more news about the timetables for those plates to stop spinning and come down, unbroken, to earth. But with a good probability that at least one of its three potentially high value opportunities will crystallise into considerably more than its current depressed market cap – albeit not immediately – I think MNC is as good a candidate as any for an investor’s Bottom Drawer, if not for his ‘Pending Soon’ tray. Into the latter could drop at any moment a strategic partner for Los Calatos.

Comments (0)