Gold stocks update – another look at Anglo Asian and Hummingbird

With gold still on the rise, mining guru John Cornford revisits two old favourites with the punters and introduces readers to two new ones as well.

What about those ‘established’ gold miners like AAZ and HUM I was wary of because they are running out of gold resources and need to spend to replace them? How much will higher prices for their remaining gold reserves prolong their lives or deliver more cash to help?

And what about a few other companies seemingly well placed to benefit from any rise in gold? I will tackle two new ones, Katoro Gold and Scotgold.

With gold so strong, should I look again at producing miner Anglo Asian?

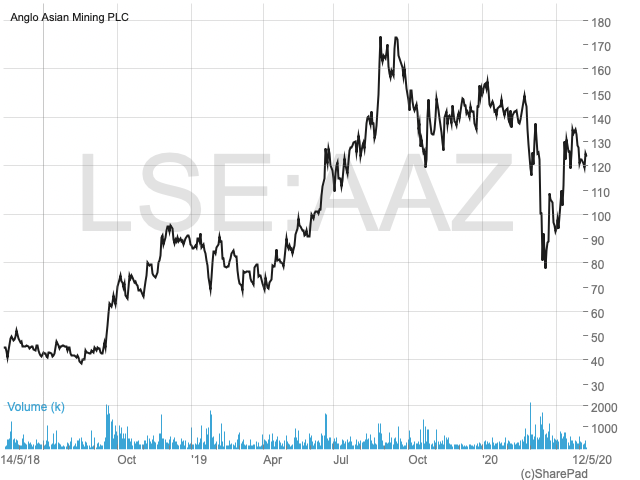

AAZ – last two years

At around 120p, Anglo Asian (LON:AAZ) shares aren’t exactly booming even though fully recovered from the Covid scare, and even though it is piling up cash. But the company has moved one year closer to the end of the life of its principle producing mine, Gedabek, whose output is slowly winding down, and AAZ’s £140m market cap probably reflects its remaining value. The short-lived spike in the shares to 160p which followed my opinion last August that it had reached its peak at 126p, was due to speculation that the Azerbaijan Government might be about to strike a new profit sharing deal to replace, perhaps with better terms for the company, the present one. That is due to run out in about three years time, after which the government will take 51% of Gedabek’s profits. Nothing has yet come of that idea.

Currently AAZ’s operations are in lock-down, but that hasn’t affected its output too much. Although, when lock-down ends, investors will note the additional $17-$20m per annum that gold, at $1,750 versus the $1,350 in the last broker valuation, will generate, I think the medium term uncertainties will limit any rise beyond last year’s 160p peak

Is Hummingbird a sweet buy at current prices?

Eight months ago I said I was avoiding Hummingbird (AIM:HUM) at 23p, but at 27p now and with gold 35% higher, I’m changing that opinion on the assumption that gold will continue on upwards.

My reservations were similar to those for Anglo Asian, in that HUM’s Yanfolila mine in Mali was running out of ore, while the cost to replace or extend it was looming.

Hummingbird – last two years

Since then, HUM has had considerable success in pushing Yanfolila’s life to at least 2025, by when it forecasts an average of over 110,000 gold ounces will have been produced per annum at a cost of under $900/oz. That compares with over a $1,300/oz cost a year ago, so that with gold now much higher Yanfolila’s profitability and cash generation is improving markedly. That has already enable HUM to bring down the borrowing to finance Yanfolila that, last year, was standing at above $50m, to under $35m now and forecast to be fully repaid next year.

On the other hand, apart from the costs to extend Yanfolila which now look more productive than they were, the cost to develop HUM’s follow-on project at Dugbe in Liberia also looks more worthwhile in light of a healthier gold price. Dugbe is larger that Yanfolila, but with lower grades and at $1,300/oz gold was looking much less profitable, and would not have been able to attract the same generous funding terms as did Yanfolila. Now, although there is still a large, $212m, capital cost to be found, its economics are looking much better with an IRR of 43% at $1,500/oz.

So, while the shares sinking to below 20p in December justified my previous caution, HUM’s prospects have been steadily improving, and I now rate it a better and longer term recovery buy than AAZ.

Two New Ideas

Scotgold

Scotgold – last two years

Another stock which, on paper, looks very cheap – and even cheaper if gold continues up – is Scotgold (LON:SGZ), the only potential commercial gold miner on the British mainland. Investors will know that Scotland and Northern Ireland lie on a very high-grade gold trend (I wrote about ‘Celtic Gold’ in August 2016) that extends between Norway and Newfoundland. In addition to high gold grades, the attraction is operation in a benign UK jurisdiction.

Among these Celtic mines are the profitable 2Moz Curraghinalt gold mine in County Tyrone, bought out at 86p two years ago from Canadian listed Dalradian Resources (whom I had flagged up 2 years before at 46p) by Orion Mine Finance.

Another is Cavanacaw nearby, owned by Galantas Gold, which hopes to resume full mining soon (having been suspended since 2013) if only it can get around various planning delays and gain funding. Talk is that it may merge with or be bought out by someone else.

Scotgold is Australian listed and bought the Cononish project in Scotland’s Grampian Mountains (in a National Park which didn’t help planning permission) in 2007, but it has taken until now to be on the verge of production. That was planned for last January, but has now been deferred indefinitely by the Covid lockdown (as well as by Scottish weather).

Along the way, delays, and re-hashes of the mining plan, along with cost increases and unforeseen hurdles, have led to a horrendous expansion of shares in issue, which now number 25 times more than in 2014, having doubled in the last two years.

At the last update of its economics (with gold at $1,200/oz) Cononish’s pre-tax 10% NPV (over a nine-year mine life) had become £53m after tax, against a then £17m market value, though the attraction diminished when the shares promptly doubled after the announcement. At 50p now, the company is valued at £26m, which would not have looked particularly cheap had gold not rocketed by $500/oz subsequently.

Again, on paper, the extra value of the approx 180,000 ounces of gold to be extracted over nine years – after tax and royalties – will be over £60m, pushing the NPV to over £100m. At the $3,000/oz gold price that a well known bank has recently predicted, you can add another £160m to that £60m.

So why aren’t investors rushing in?

The answer is that, after all the delays and cost increases, many don’t trust the management. Just four directors own 70% of the shares, while a £6m loan to the company from its chairman, recently arranged to tide the company over yet more delays and cost increases, has first call over its assets which, if the project goes bust, they can take over.

I, personally, think the market’s reluctance is overdone. If gold holds up, and Scotgold does get going, it will look really cheap. There are some issues however that might slow (but not necessarily stop) any share progress.

1) Investors fear another share issue soon, despite the £5m ‘tide-over’ loan.

2) The mining plan is split into two stages, whereby half scale production for the first three years is followed by more investment (planned to come from phase one profits) to enable a ramp up to full production from year four onwards.

4) Before reaching its valuable high-grade ore and the resulting high profits, the mine has to slog through more low-grade ore than expected for the first two years, so that funds for the second stage investment might be delayed.

But if investors are convinced that gold will continue strongly upwards, I think they will give Scotgold the benefit of the doubt.

Katoro Mining

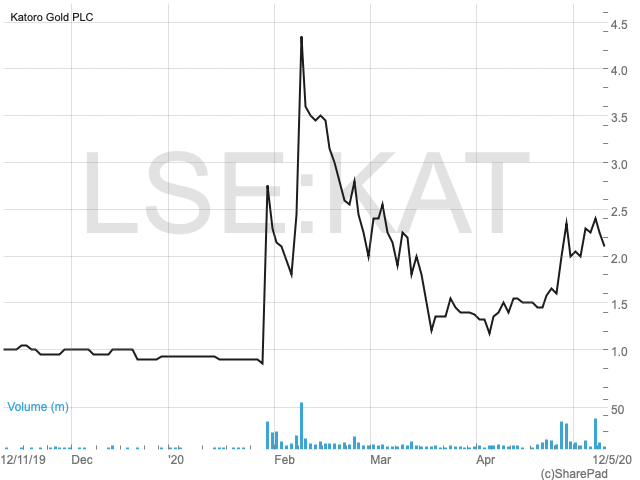

KAT- last six months

Katoro Mining (LON:KAT) is a spin-off from Kibo Energy (the coal to power stock I have repeatedly advised investors to avoid) whereby it took over Kibo’s remaining gold and nickel mining prospects, and listed separately three years ago with 108m shares at 6p, Kibo retaining 56%.

Subsequently the usual Kibo mismanagement saw KAT sell off its gold mining operations at a sharp loss, with the shares collapsing to around 1p. But in January it announced a potentially transformational deal.

By collaborating 50/50 with South Africa’s Blyvoor Gold, KAT proposes to recover, over 25 years, some of the 1.3m ounces of gold currently locked up in Blyvoor’s tailings dams. On the 53% recovery assumed, Kat’s share at a $1,750/oz gold price would be worth $600m compared with its current market cap of only £5m.

The deal has not yet been formally agreed, and signing has been delayed due to the Covid lockdown, but the main reason the shares have not yet fully reacted is that there are some key issues to be resolved. These centre on whether KAT can, as required by the terms, find the required capital investment, and the amount required to start the project at an initially lower recovery rate. As far as KAT is concerned also, is the question of the other exploration business that it has retained, and how much it will cost shareholders to develop.

A detailed economic analysis for the tailings has only just been published (differing somewhat from the details mentioned with the January announcement) showing that over 25 years, 661,000 gold ounces should be produced, at an all-in cost (ie including capital) of $920 per ounce. At $1,500/oz that will generate a 5% NPV of $131m (or $94m at the usual 8% discount rate) and a 25% irr which, for a miner, is good but not as startling as one might expect from what private investors might think should be a simple operation. Achieving $1,750/oz will obviously make the figures look much better.

That the operation is not simple is shown by the total capital cost needed throughout its 35 year life, which amounts to $110m ( 3 times what was mentioned in the initial January announcement). Of that, a peak requirement of $36.4m will be required at some point – probably a few years in, when an initial smaller operation is expanded.

Those figures are before any costs of finance. The January announcement assumed that KAT would raise it by debt, but that appeared to be assuming an initial capital cost of only $11m, so, with the updated figures, that may not be possible and Kat might also have to issue shares – how many we cannot yet guess.

Before we know, preliminary planning work was stated to require up to $800,000 funded by loans convertible into KAT shares at 1.4p. Some have already been converted, and if all are, the total in issue will be 267m.

If the initial required capex is in fact $36.4m, raised by debt, the cost of its repayment over ten years at 10% interest would be equivalent to an 8% NPV of at least $40m, which will detract from the $94m I have calculated above.

So the net 8% NPV per current KAT shares in issue on that basis turns out to be 20p.

Without more detail, these estimates have to be extremely crude, and readers will know my opinion (based on experience) that share prices never reach more than half their theoretical NPV based value. That means on present knowledge that I wouldn’t place more than a 10p value on the shares, even once the project gets started.

There is also one other issue to consider, apart from whether the tailings project will happen at all.

KAT still has (and makes much of) its nickel exploration prospects in Tanzania. Kibo held them for many years and, while initial ‘desk’ research has promised possibly large nickel deposits, and KAT has a partner bearing part of the cost, two other joint venture partners, including a world nickel major, Brazil’s Votorantim, pulled out a few years ago after an initial look. And currently the nickel price isn’t far above all-time lows.

Shareholders will hope that KAT will not have to pour funds into nickel, and at the same time have to raise equity for the tailings project.

Currently, the key question is whether KAT can raise the funds. Even though it is encouraging that a highly experienced former manager of major miner Harmony Gold has been appointed to manage the tailings project, the following standard disclaimer is, I think, more appropriate than usual. If the project doesn’t happen, KAT’s shares will be practically worthless.

“Katoro shareholders should be aware that there is no certainty that the projected returns set out above for the Project will be achieved, as there is no certainty that the Project Funding will be secured and if it is secured, that debt funding will be secured to finance all of the projected costs of the Project and if the Board is able to secure such debt funding, that it will be in line with the Board’s current expected rates, in which case the Project’s returns, as set out above, could be materially impacted resulting in the Project not being economical. In addition, if the Project Funding is in the form of a mixture of debt and equity, as opposed to just debt as currently proposed by the Board, it is likely that the Parties interest in the JV will be diluted and the Company’s interest in the JV could therefore be materially lower than 50%.

Also, there can be no guarantee that in the event that the Tailings are reprocessed, that the projected

production and/or recovery rates will be achieved, or that the targeted 500,00tpm of material within two years will be achieved, which could result in lower returns and which may require additional funding to be secured, which could result in the Company’s interest in the JV being reduced.“

I am amazed that a new mine is allowed in a Scottish national park, its absurd.

It doesn’t seem a safe juristriction to me.

Ref ….. Scotgold.