Looking beyond a 60/40 portfolio

For a long time, a 60/40 split between stocks and bonds has been thought of as a balanced portfolio and the best way of investing for the longer term. However, the balance changes, as the correlations between stocks and bonds change.

Investing is a game of greed and fear, which is influenced by age, financial situation, personal objectives and a other circumstances. Traditionally, the equity part of a portfolio returns a lot more than its fixed-income counterpart, in particular over long periods of time. However, stocks are riskier and exposed to much deeper drawdowns. This is a good reason to reduce equity exposure. But not all situations are the same. Younger investors may benefit from increasing exposure to stocks because at the age of 20, 30 or even 40, there’s plenty of time to recover from a drawdown before retirement. Older investors, nearing retirement age, cannot afford such risk, so may prefer tilting their portfolio towards fixed income. In between these two extremes lies the 60/40 split, usually viewed as a balanced portfolio and often used as an investment rule.

Diversification is key

Diversification is a key metric derived from the work of Harry Markowitz, who created the foundations of the Modern Portfolio Theory (MPT). The idea is that we shouldn’t rely solely on expected returns but instead look at the risk-return relationship. As long as assets do not correlate 100%, we can reduce the risk of a portfolio by adding them together. Even adding assets to a portfolio just for the sake of increasing the number of holdings works well as a risk-reducing strategy. In the end, an efficient investment strategy includes a portfolio composed of higher-risk assets and a risk-free asset. Our own preferences will then dictate how much of the higher-risk assets we want, with younger people in general looking for more and older people taking less.

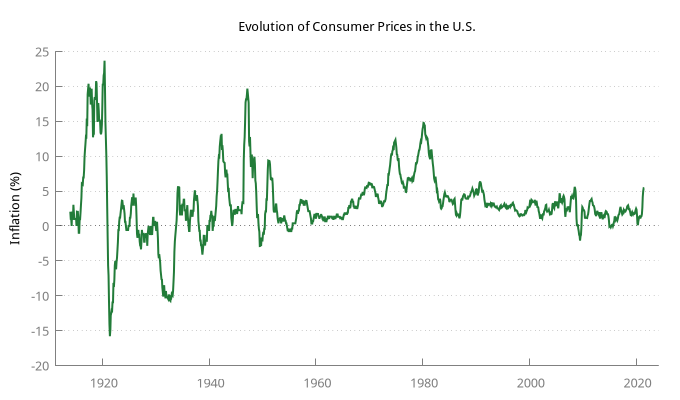

A key concept behind MPT is the correlation between assets. Correlations vary between -1 and +1. Diversification is particularly powerful when correlations are near zero. For years, the correlations between bonds and stocks have been slightly negative to near zero, which provided great benefits for investors holding balanced portfolios of stocks and bonds, in particular the traditional 60/40 holding. This has been happening for the last two decades but not before then. Bonds and stocks previously had a positive correlation, in particular at times of higher inflation.

Inflation has been declining since the 1980s and has remained below 2% for most of the last two decades. It was even negative for a few months in 2008 and 2015. However, it has been accelerating this year and its current reading is 5.4%, a figure not seen since the pre-financial crisis period of 2008. Central banks have spent the last 15 years trying to revive inflation by keeping interest rates near zero (when not negative) and by injecting massive amounts of liquidity into the economy through asset-purchase programmes. With inflation finally showing up, central banks will most likely live comfortably with rising prices, as long as the rise is just moderate.

Can bonds still offer a good hedge?

As a consequence of low interest rates and dovish monetary policy around the world, for so long, asset prices eventually increase to ‘bubble’ levels. It’s hard to tell whether a bubble exists, before it bursts, so I can’t say if we have one right now. However, stock prices have been rising for longer than during most previous bull markets. Price earnings (P/E) ratios are very high, in particular in the US (they are not so stretched in the UK). The S&P 500 and the Dow Jones 30 currently trade on a P/E ratio of 30.04 and 23.31 respectively. Even though these figures have been improving a little, they’re still very high by historical standards. The dividend yield for the Dow is 1.86%, which is very low to say the least.

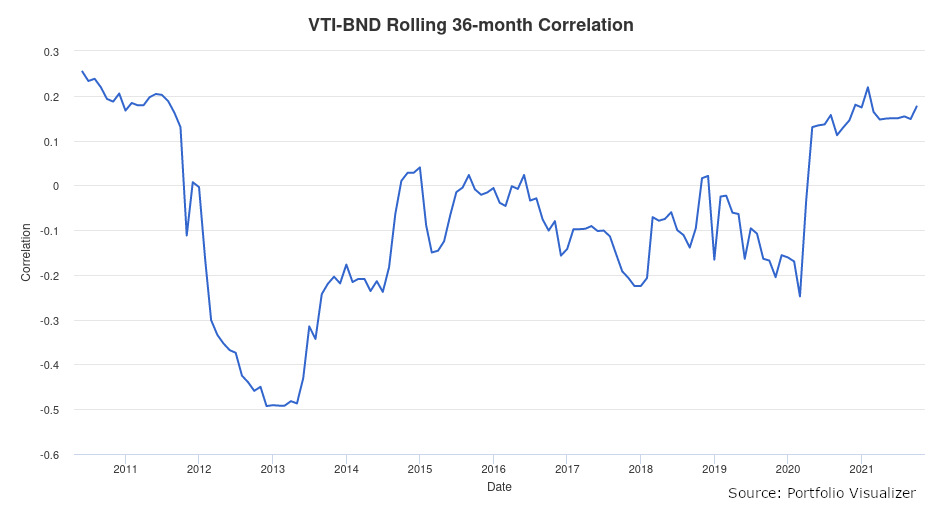

When you invest in a 60/40 portfolio you expect bonds to protect you from big drawdowns. This is exactly what happened in 2008. While a portfolio fully invested in stocks lost 37% that year, a 60/40 balanced portfolio lost 19%, as bonds performed well that year. But that happened because the correlation between stocks and bonds was negative and slight. The big question is: should we expect it to stay that way?

The chart above shows the rolling correlations between VTI and BND over time. VTI and BND are two broad-based Vanguard ETFs that represent the full US market for stocks and bonds respectively. In 2013 the correlation between these two ETFs was around -0.5, declining to near zero by the end of 2014 and remaining at that level for most of the period up to the beginning of 2020. This is an ideal situation for diversification purposes.

However, correlations have been on the rise since the start of the pandemic. Prices for both stocks and bonds are elevated due to past central-bank intervention and they are exposed to corrections in the same direction. For this reason, I believe investors should look into alternative asset classes to get some diversification. VTI and BND are a good starting point for a balanced portfolio, but you can add a few more layers. Vanguard predicts a median annualised return of 3.2% for the S&P 500 over the next decade. The yield on a 10-year Treasury bond is currently 1.50%. The scenario for the 60/40 portfolio doesn’t look appealing.

A few alternative investments

WisdomTree Alternative Income Fund ETF (BATS:HYIN)

The WisdomTree Alternative Income Fund (HYIN) tracks the the Gapstow Liquid Alternative Credit Index (GLACI). It is comprised of debt securities whose yield or expected return is higher than investment-grade fixed income securities and includes a range of securities across a broad universe of borrower segments, such as corporations, households and commercial real estate sponsors.

The ETF invests in publicly-traded alternative credit vehicles (PACs), which are the subset of business development companies (BDCs), closed-end credit-centric funds (CEFs) and mortgage real estate investment trusts (REITs) that specialise in alternative credit investing. In summary, investors have access to a private debt market giving access to floating-rate, senior-secured loans to small to medium businesses; syndicated leveraged loans; collateralised loan obligations; and residential and commercial mortgage-backed securities, among other types of alternative credit. The appeal of all this is the 8% yield, which compares with 1.50% on a 10-year Treasury bond. It even has the advantage of being much less sensitive to changes in interest rates because its duration is very low. HYIN was launched this year, at a time when investors have been looking more and more into private credit as an alternative fixed income asset.

Invesco Global Listed Private Equity ETF (NYSEARCA:PSP)

The Invesco Global Listed Private Equity ETF is based on the Red Rocks Global Listed Private Equity Index. PSP invests at least 90% of its total assets in American depository receipts (ADRs) and global depository receipts (GDRs) of 40 to 75 private equity companies, including BDCs, master limited partnerships (MLPs) and other vehicles whose principal business is to invest in, lend capital to or provide services to privately-held companies. The ETF and the corresponding index are rebalanced and reconstituted quarterly. PSP offers access to a market that retail investors aren’t usually able to access because of the high amounts needed to enter. It currently has 83 holdings.

Vanguard Real Estate Index Fund (NYSEARCA:VNQ)

In previous articles I have suggested real estate and property-related stocks as a good investment because they offer good diversification benefits. Also, real estate has been performing well under the current economic conditions. VNQ invests in stocks issued by REITs, companies that purchase office buildings, hotels and other real property. VNQ generates income in addition to any capital appreciation and is a very good hedge against inflation. It provides access to some of the biggest residential, commercial and industrial real estate companies in the US, including mall operator Simon Property Group, apartment developer AvalonBay Communities and telecom giant American Tower Corp.

Global X SuperIncome Preferred ETF (NYSEARCA:SPFF)

The Global X SuperIncome Preferred ETF (SPFF) invests in 50 of the highest-yielding preferred stocks in the US and Canada. It makes distributions on a monthly basis, which is unusual but an excellent option to help investors generate periodic income without selling assets. The current 30-day SEC yield is 5.21%. SPFF provides access to preferreds − a hybrid between a stock and a bond. It provides higher and safer dividends than a share but without voting rights. These instruments are in general much less volatile than stocks.

Cryptocurrencies

While I don’t entirely endorse the cryptomarket, due to a lack of legislation and questions of fundamental value, we can’t ignore the rise of its market capitalisation from $12.2bn to $1.3tn over the last five years. This market is growing very fast and is currently on the radar of several institutional investors like Cathie Wood of the ARK funds and Michael Saylor of MicroStrategy.

The crypto market, which started with Bitcoin more than 10 years ago, currently features more than 3,000 different tokens. A lack of legislation makes this market riskier than any other for investors but a few ETF funds investing in Bitcoin and Ethereum already exist outside the US and this will most likely increase, globally. The biggest digital coins are Bitcoin, Ethereum, Cardano, Binance Coin, Solana, Ripple and Polkadot. While each project has its own merits and features, they have one thing in common: they all offer good diversification benefits to a traditional portfolio allocation. The correlation between these digital coins and the S&P 500 has been around 0.25 for the last year, which is relatively low. Even more important is the fact that the correlation between Bitcoin and Gold is near zero, which means Bitcoin is not a replacement for gold but rather a complement. They may coexist in the same portfolio for maximum diversification benefits.

Final words

Uncertainty about future inflation and the small income provided by bonds may contribute to rising bond volatility. Predicted performance for both bonds and stocks is poor for the next 10 years and a potential rise of consumer prices cannot be discounted, which would turn bonds into a burden and may change their correlations with stocks into something less favourable in terms of diversification. For this reason, investors are already looking into alternative asset classes like private credit (and equity), real estate and crypto. These are risky assets but may provide a new layer of diversification and enhance the predicted low portfolio returns that are expected from a balanced 60/40 portfolio.

Comments (0)