7 strategies for boosting UK tracker returns

In the first of a seven-part series for Master Investor, Glenn Martin, author of 7 Successful Stock Market Strategies, discusses seven strategies for boosting UK tracker returns.

Over the last 10 years UK equities have outperformed all other non-physical UK asset classes, producing a real annual return of 4.1% compared with the miserable negative return from cash of -0.7%.* Furthermore a recent study by fund manager Barings predicts that UK equities will be among the best performing global assets over the next 10 years.

So what is the best way to invest in UK equities? There are 3 main options:

- Individual UK shares. Running a share portfolio requires a lot of effort and involves significant risk. For example, once highly respected companies such as RBS, BP and Tesco have suffered plunges in their share prices through unforeseen dramatic events.

- Commercial share funds. Only a handful of funds consistently outperform the market and there is no guarantee that they will do so in future.

- Index funds These aim to replicate the performance of an index such as the FTSE 100 or FTSE 250. I believe that index tracker funds are the most suitable option for a personal investor to invest in UK equities. The popularity of these funds has grown enormously in recent years and, because of intense competition, the management fees have fallen sharply.

You should be able to achieve better returns than just tracking the market. My new book, 7 Successful Stock Market Strategies, details seven strategies for boosting tracker fund returns. Two unique systems underpin the strategies:

- Market valuation system

This system values the FTSE 100 in comparison with its market price. The book explains step by step how you can build a spreadsheet to operate the system. Alternatively FTSE 100 valuations are provided automatically to ShareMaestro clients (www.sharemaestro.co.uk). A valuation over 100% indicates the value is greater than the price; below 100% indicates the reverse. These percentage valuations can be used as signals for entering and exiting the market. A proven strategy is to buy the FTSE 100 when the valuation reaches 105% and sell when the valuation falls to 95%. These timing signals can also be used for the FTSE 250, since the market turning points for the two indices are very similar, as can be seen from the chart below. The FTSE 250 is the top line.

Using these buy/sell signals since the start of each index, every buy/sell pair has produced a capital profit. Total points gained when in the market have been 6138 (17382) and total points lost when out the market have been 380 (1166). FTSE 250 figures are shown in brackets.

- Market momentum system

There are times when the market gets gripped by panic and prices go into freefall, irrespective of the market valuations. This system is designed to give protection against the impact of these crashes. The system uses the simple 100 day and 200 day moving average prices of the FTSE 100 (or FTSE 250), which show the underlying momentum of the markets. If the 100 day moving average crosses below the 200 day and the market price falls a further 10% from this point, you exit the market. You re-enter the market when the 100 day moving average crosses above the 200 day and the market valuation is above 105%. You can get moving average charts free from services such as Digital Look.

The example below shows the system in action for the credit crunch crash. The moving average lines are the smooth lines and the jagged lines are the actual market prices. The market exit occurred on 21 January 2008 at a price of 5578.2. Market re-entry occurred on 28 July 2009 at a price of 4528.8. The system therefore avoided 1049.4 points of the crash.

The system has been triggered only three times in the history of the FTSE 100 since other crashes occurred when the market valuation system had already triggered a market exit.

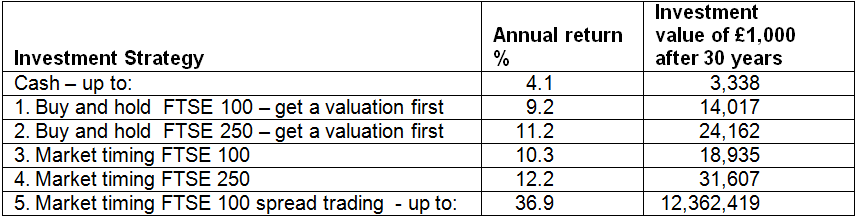

Strategy returns

The table below summarises the long-term returns of my strategies, from the start of the FTSE 100 and FTSE 250 indices (in 1984 and 1986 respectively) to the end of September 2014. The returns include reinvested dividends and take into account all costs, including basic-rate income tax. The final column shows the investment value of £1000 after 30 years compounded it at the annual rate of return.

The return from strategy number 6 – Market timing FTSE 250 spread trading – is not quoted because historic FTSE 250 spread trading prices are not available. Strategy number 7 does not have a specific return since it is a technique for creating a tax-free FTSE 100 tracker fund.

Index trackers are not suitable for short-term investment (up to 5 years) since index values can fall over short periods. However the long-term returns of these strategies are very strong. Even the lowest return produces a 30-year fund value over quadruple that of the cash fund. The addition of the market timing systems, which I have described above, adds over 30% to the long-term fund values. It is also noticeable how much the FTSE 250 has outperformed its big brother, the FTSE 100.

Summary of the strategies

Strategies 1 and 2 are the simplest and suitable for novice investors– buy and hold an index tracker fund, reinvesting the dividends. However it is essential to conduct a market valuation first to ensure that you are not buying at the top of the market. An investment at the end of 1999, when the FTSE 100 valuation was only 56%, would have taken 7 years to recover its original value, including reinvested dividends.

Strategies 3 and 4 incorporate the market valuation and momentum systems to switch between index investments and cash deposits.

Strategy 5 is the most complex strategy. It uses the market timing systems to switch investment between FTSE 100 spread trades and cash deposits. Because it uses the leverage offered by spread trading, it is also the riskiest strategy in the short term and therefore incorporates various risk controls. However the long-term returns can be spectacular and better than any long-term hedge fund returns.

Over the coming months, I will be writing a series of articles in Master Investor, describing each strategy in more detail. I will also explain the different types of index funds available and recommend those that are most cost-effective for long-term strategies. If you choose the wrong type of fund, you could pay annual charges of 0.45% in addition to the internal fund management fee. This may not sound a lot but would amount to £450 a year on a fund of £100,000.

* Source: Barclays 2015 Equity Gilt Study

Sharemaestro seems to exist as a web site but says it has closed down its service, any ideas why? Doesn’t seem to have updated in several years