Budget 2017: Mr Hammond’s timely reprieve

UK government finances are under extreme pressure. But there is no need to panic – yet.

Chronicle of a death foretold

Mr Hammond, Chancellor of the Exchequer, rose to the despatch box on Wednesday like a condemned man given one last chance beneath the gallows to plead for his life. It would have to be an oration of such extraordinary potency that the bloodthirsty multitude might cry out for clemency…

The mood in the Tory Party is sanguine: another cock-up budget like the last one (when hikes in NICs for the self-employed had to be reversed within weeks) would have spelt the end for Mr Hammond – and possibly for the fragile May government itself. (Though exactly what might replace it is the overwhelming question.) A do-nothing budget would also have gone down badly.

In the event the Chancellor bravely managed to disguise the immense pressure on UK public finances with a gloss of positive statistics. The budget speech of 7,843 words was delivered with good humour, some panache and mercifully without any coughing fit. The condemned man repaired from the gallows unhung, the bloodthirsty multitude in mute applause.

I am assuming that my readers will already have digested the major features of the 2017 budget – so I shall just focus here on three strategic themes that will impact the markets going forward.

The productivity conundrum

The most important point about this budget was that UK GDP growth forecasts for the next five years have been slashed by the Office of Budget Responsibility (OBR) with huge attendant consequences for the fiscal deficit, government borrowing and the total projected level of the national debt. The OBR cut the projected growth rate for 2017 from 2 percent to 1.5 percent. It now thinks that the UK economy can only grow sustainably at 1.5 percent.

This is because, in its wisdom, the OBR has determined that productivity is likely to grow in the next five years by much less than its historic average. It believes this because productivity growth in Britain has been lacklustre since the Credit Crunch and the subsequent recession of 2008-11.

Thus the Institute of Fiscal Studies (IFS) declared on Thursday that, based on the OBR figures, the outlook for the British economy is “grim”. They released a lot of unhappy charts concerning disposable incomes. Canny readers will know that the IFS is the provisional wing of the OBR.

For more insight and analysis like this, CLICK HERE to read Master Investor Magazine for FREE.

It is widely said that the UK is undergoing a productivity crisis. The often cited received opinion is that our productivity is 30 percent or so below the German level. But there are reasons to suppose that this particular omelette has been over-egged.

First of all, there is the problem of measuring productivity. It is childishly simple to compare the relative productivity of two factories which both produce standardised widgets. The one that produces the most widgets in a month (or whatever timeframe chosen) is the most productive. But most manufacturing these days is customised: for example, every car that rolls off a modern production line has a different specification to the one that preceded it because virtually all cars are made to order. Customisation of product makes the direct comparison of two factories’ outputs trickier. So even in the manufacturing sector there are problems in measuring productivity based on output.

Now there is no question that Britain boasts some centres of excellence in manufacturing. The Nissan plant in Sunderland is reputedly one of the most efficient car plants in the world. The Airbus wing production plant in Broughton is regarded as a benchmark in the global aerospace industry. Rolls Royce’s (LON:RR.) aero engines compete hard with those manufactured by Pratt & Whitney (owned by United Technologies (NYSE:UTX)) – and so on. The matter is that Britain has a larger portion of the economy than France or Germany characterised by low skills and low wages – for reasons I shall explain.

Secondly, the British economy is an interesting example of the 80:20 principle: it is composed roughly of 80 percent services and 20 percent manufacturing, construction and agriculture[i]. (It has a very similar economic structure to that of France, though France has a much larger agricultural sector). If measuring productivity in the manufacturing sector is not straightforward, measuring that of the services sector is highly problematic.

Is WPP (LON:WPP) a more productive advertising company that Omnicom (NYSE:OMC)? We can easily calculate revenue per employee – but that is not the same thing as productivity. Or indeed, what about writers? If I can tap out more words in an hour than my distinguished colleague Nick Sudbury, does that make me more productive than he? If so, is Evil Knievel’s elegant concision a sign that he is underperforming? In which case, does he require upskilling? (I doubt it.) You get my point.

The third point is that over recent years the UK has been extremely successful at creating jobs. The lower unemployment falls the more you will tend to draw lower skilled people into the workplace and thus the lower output per head will be. France enjoys higher productivity than the UK; but it has persistently suffered from much higher unemployment over many years. Currently, the unemployment rate in France is 9.8 percent[ii] against 4.1 percent in the UK. So in fact we could probably raise our productivity overnight to near French levels if the government passed a decree declaring that two or three million baristas be fired forthwith – though admittedly that would cost the government in terms of welfare payments.

The reason that more low skilled workers have been able to find work in the UK is threefold. Firstly, we have a more flexible labour market than either France or Germany. And second, as a corollary to that, we have attracted more low-skilled migrant workers from Eastern Europe where labour rates are lower than here. The second factor has had the effect of depressing wages at the lower end of the pay scale and ipso facto of reducing productivity. Thirdly, it is much easier to become self-employed in the UK than in France or Germany: in fact we have between four and five million people in this category.

Don’t miss Victor’s new piece in the next edition of Master Investor Magazine – Sign-up HERE for FREE

That is why some economists who incline towards the Right believe that there is a strong case to increase the Living Wage to a level much closer to median incomes – perhaps to £12 in the UK right now. That, at a stroke, would increase productivity; but it would also impact corporate profits (and therefore corporation tax receipts), inflation and returns to shareholders. Also, many marginal businesses (much of the High Street, then) would simply die.

The other important factor in which to contextualise this discussion is that the rate of growth of productivity seems to have stalled across the Western world. The American economist, Robert J Gordon[iii] argues in his book The Rise and Fall of American Growth that the rate of technical progress has fallen as the world has run out of epoch-changing inventions and technical innovations. He argues that although the recent communications revolution – the internet, smartphones and social media – has transformed our lives, it cannot be compared with the first industrial revolution which brought us the steam engine and the railways; or even with the second industrial revolution which brought us the internal combustion engine, cars, electric power and air travel.

I have reservations about Professor Gordon’s argument. One competent entrepreneur can run a small business today using the internet and a laptop – undertaking tasks (bookkeeping, invoicing, advertising etc.) that would have required a dozen people 40 years ago. Moreover, we are about to enter a fourth industrial revolution with the advent of Quantum Computing (QC), Artificial Intelligence (AI), and robotisation which could accelerate productivity growth more than we can now conceive. (Not that that will be much consolation to poor Mr Hammond.) The fact remains, however, that the greatest impact of the communications revolution came at its very beginning over the period of roughly 1993-98 – when the economies of Europe and America grew strongly, along with their stock markets.

Furthermore, international comparisons of productivity tend to ignore the public sector. Teachers, policemen and doctors will tell you that they are desperately underfunded, and I would not argue with them. But what they really mean is that they are required to do so much more than their forebears did twenty or thirty years ago. On the plus side, interaction between citizen and government – renewing a passport, paying one’s road tax, applying for planning consent – has been revolutionised by user-friendly internet portals. In my personal experience the UK is way ahead of its European peers in this domain.

One reason why the rate of productivity growth in the West has slowed is that the rate of capital investment has fallen since the Credit Crunch. The reason for this is that near-zero interest rates have prevailed. Lower borrowing costs also imply lower rates of return on capital, thus reducing the incentive to invest. Near-zero interest rates encourage capital to be misallocated into unproductive activities and permit zombie companies to keep going. These zombies pay the lowest wages and have the lowest levels of productivity. (Cupcake shops spring to mind; though, mercifully, these have now largely been culled.)

One way to boost productivity over the medium term will be to improve educational attainment. But, as Mr Hammond told John Humphrys on BBC R4’s Today Programme on Thursday, if you improve maths teaching today, that will take many years to feed through into higher productivity. As a matter of fact, maths grades are improving in England and Northern Ireland, though they have been falling in Scotland of late where education is a devolved function

But, ultimately, the Chancellor has to plot the course of public finances in accordance with OBR numbers – even if the OBR’s assumptions about future productivity growth are about as scientific as a Nigella Lawson recipe for Christmas pudding.

The debt burden

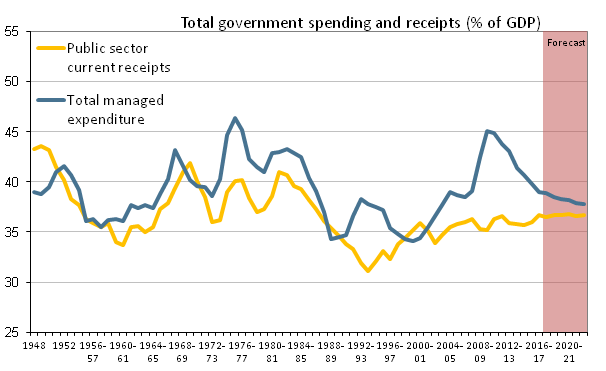

Despite the gloomy outlook envisaged by the OBR Mr Hammond increased spending. Not to have done so would have enraged the multitude. Tax receipts are holding up well but the deficit will still be in the order of £50 billion this year or about 2.4 percent of GDP. The Treasury got a £9 billion windfall this year from a lower borrowing forecast, but the impact of the OBR projections is that tax receipts by 2020-21 will be £20 billion less than previously forecast. The deficit will still be running at around £26 billion or 1.1 percent of GDP by 2022-23[iv].

Government spending will exceed the £800 billion mark next year (2018-19) for the first time – but that will “only” be 38.5 percent of GDP as compared with 54 percent of GDP in France. To be fair to the Chancellor, spending is converging with tax receipts (see chart). Borrowing is now forecast to be £12 billion higher in 2021–22 than was forecast in March. So the deficit is still declining but much more slowly than previously forecast. Mr Hammond’s key focus therefore is the headline debt-to-GDP ratio. This, he says, will peak this year at 86.5% of GDP, and then fall in every year thereafter, reaching 79.1 percent of GDP in 2022-23.

The most frightening part of these forecasts is the absolute level of debt that the government continues to accumulate. The national debt stood at around £750 billion when Mr Brown vacated Number Ten; today it stands at around £2 trillion; in 2023 it will reach almost £2.5 trillion. Please don’t look at the charts – it’s upsetting. Our children will never unburden themselves of the millstone that we (collectively – though I have always warned against it) have placed around their necks.

We should recall that all of this is based on econometric forecasts which are all based on the unsophisticated method of extrapolation and are always (ahem!) subject to amendment. Though there will be many who take satisfaction in the fact that Spreadsheet Phil has been hoist on the petard of his own IF function.

Encouragingly, the Pound pipped upwards and the FTSE-100 stumbled before recovering on Thursday. That was tacit approval from the markets.

It’s the politics, stupid!

It is currently fashionable to believe, as Marxists do, that politics is driven purely by economics. It’s the economy, stupid, as Bill Clinton famously barked in 1992. But in fact the economy is driven by policy decisions made by politicians who act out of short-term political motives. Mr Hammond’s real problem is not the weakness of the British economy; it is the weakness of the Conservative Party.

Ever since the botched general election of 08 June this year, from which the Tories were supposed to emerge with a thumping majority, but instead scraped back with a minority government, the Tory Party both inside Parliament and outside has fallen into the Slough of Despond. Most Tories believe that Mr Corbyn’s star is still rising and that his eventual arrival in Number Ten is all but inevitable.

This apprehension is magnified by the enormity of the task of negotiating Brexit. The earnest Brexiteers know that history will judge them harshly if there is a no-deal or a bad-deal outcome which damages the economy. The at-heart Remainers (of whom Mr Hammond is one) hope against hope that Brexit might be reversed – most likely by a second referendum on the terms of the final deal. The earnest Tory Brexiteers and the Tory at-heart Remainers loathe one another as fiercely as the Roundheads and Cavaliers once did.

For more insight and analysis like this, CLICK HERE to read Master Investor Magazine for FREE.

The Corbyn threat is relatively easy to analyse. The Tories have only just realised that Labour – or more accurately Momentum – has built up formidable firepower on social media which they feel entirely unable to emulate. Just consider that Mrs May has 411,000 followers on Twitter (NYSE:TWTR) and 540,000 on Facebook (NASDAQ:FB). Mr Corbyn has 1.6 million and 1.4 million followers respectively. One of Labour’s election videos – Daddy, why do you hate me? in which a little girl scolds her father for having voted Tory in 2017 – was watched 5.4 million times in two days[v]. Momentum created a WhatsApp cascade on polling day designed to get the votes out which was seen by an estimated 400,000 young people.

Furthermore, the demographics are against the Tories. Every year more Tories die than new voters reach 18 – the latter being overwhelmingly inclined towards Mr Corbyn.

There is even an element in the Tory Party – read the Evening Standard – which believes that only Corbyn can save us from a calamitous Hard Brexit. They will do nothing to stem the tide. And for those, like me, who believe that a Corbyn government would be a catastrophe, the Tory Party is just not up for the fight.

It is easy to blame Mrs May for the election debacle, given her presidential tone at the start of the campaign, her failure to engage in the TV debates, the entirely unnecessary flip-flopping on social care, the totally underwhelming manifesto – and so on. But Mrs May presided over a Dad’s Army of enthusiastic but unprofessional volunteers who, though no doubt doing their best, were totally outgunned by Labour’s social media-savvy storm troopers. Local Tory associations used to be manned by bumbling gentlemen in tweeds and nice ladies in funny hats; now they rely on a dwindling band of part-timers. Try telephoning your local Tory Constituency Association: there will be nobody there. The Tory Party on the ground is a hollowed-out gerontocracy with declining membership. They don’t even hold sherry parties anymore.

This weakness is compounded by a lack of necessary talent and political experience within the ranks of the government itself. When the Cameron-Osborne pantomime horse sadly limped off the stage it took with it a residue of strategic thinking about the management of the country’s finances. Notwithstanding my criticism of Mr Osborne, the direction of financial policy over 2010-16 was the right one.

Meanwhile, British households face an unprecedented 17 years of stagnation in wages at a time when consumer price inflation is at three percent, largely as a result of the weak Pound. Mr Osborne’s plan for five years of austerity that would restore the nation’s finances to good order is now set to be at least a 13 year stretch – and counting. There is no end in sight for the age of austerity.

On such a battlefield, Mr Hammond could only, at best, hold the line. The budget is not just an occasion on which the Chancellor announces the tax rates for the following year: it has become a set-piece event in which the government’s entire strategy, economic and social, is paraded with fanfare. Thus, policies relating to reducing plastic pollution in the oceans, alleviating the impact of Universal Credit, planning policy, provision of housing and the tightening of tax loopholes were presented. It is therefore more about psychology than numbers. And overall, the Tories’ mood has lifted.

But the glorious day when the books will balance and accumulated surpluses pay down the national debt recedes further into the distant future. For the first time since 2010, the Chancellor did not even specify a date for that epiphany. A Treasury official, when asked about this by The Spectator’s Chairman, Andrew Neil, vaguely mentioned 2032[vi].

Someday, over the rainbow…

Let’s pray the gilts market can wait that long…

[i] See: https://visual.ons.gov.uk/five-facts-about-the-uk-service-sector/

[ii] July 2017 figure.

[iii] He is the Stanley G. Harris Professor of the Social Sciences at Northwestern University.

[iv] All figures here from: https://www.gov.uk/government/publications/autumn-budget-2017-documents/autumn-budget-2017#economy-and-public-finances

[v] See Corbyn 2.0, by Robert Peston, The Spectator, 18 November 2017.

[vi] Spectator Budget Briefing, 22 November 2017.

What are cupcake shops that have now largely been culled?

Productivity: the clear superficial short term benefit of the U.K. policy is low unemployment.

However, it has caused a large proportion of people to be in low paid, part time, insecure work, and so resentful. This is bad for society: note the vote for Leave EU and Mr Corbyn.

In economic terms, it places the UK as a competitor of third world countries; where we are bound to lose due to the cost of welfare.

The solution is to create specialist ‘high tech’ industries with skilled labour. To achieve this requires:

(1) incentives to business to invest. As the article says, these are absent. Could HMG not change this? Regional development plans, tax incentives, etc.

(2) a better educated work force. As the article says, this will take time; but again there is much HMG could do: encouraging universities and prospective students to promote science courses, enabling older people to rest ill through short courses, and radically changing the attitude in schools.

Being older it is not a problem for me; but we let down young people. Nonsensical comments about baby boomers stealing from the young are (deliberate?) distractions. We all want a better economy and society. Putting politics aside, the present government is without hope or competence, while the alternatives are frightening.

Thanks for the analysis of the difficulties of measuring productivity. But aren’t the statisticians aware of these points? If one of the main reasons for the “productivity” gap is really the UK’s high employment rate, why don’t the statisticians simply correct for this? And why don’t they intervene and call out all the people like Shadow Chancellor John McDonnell, who are making political capital out of such misinterpretation and claiming the solution to the nation’s problems is a massive expansion of state capital investment and big pay rises for the public sector workforce?

Erm, would Victor also please explain why “lower borrowing costs also imply lower rates of return on capital” and why this discourages investment? Don’t lower borrowing costs make for a higher return on capital investment, simply because the business or person making the investment has to waste less money on interest charges? If Project X has an estimated rate of return of 10% p.a., and borrowing to help fund the investment costs 5%, why is this more attractive than with borrowing costs at 1%?

Similarly companies are holding trillions in cash. With interest rates so low, why isn’t this cash being invested, or returned to shareholders, or used for takeovers? The very high corporate tax rate in the US, which is supposedly causing multinationals to hold their non-US profits in cash outside the US rather than repatriate it, can’t be the only explanation for all these assets being held in the form of barely-productive cash.

Tony – you make three important points here. (1) I will show in a forthcoming article why OECD measures of productivity are actually extremely misleading – statistics can be used in all kinds of ways – the point is to interpret them intelligently. (2) Your point about ROC and interest rates – forgive me, but you have put the cart before the horse, here. Interest rates track the rate of GDP growth plus inflation – though since the “Credit Crunch” that relationship has broken down for reasons that I have discussed and will continue to ponder…The rate of GDP expansion in turn tracks the rate of ROC over the medium term…Therefore, I maintain that super-low interest rates (sustained over time) IMPLY that the overall rates of ROC have fallen. (3) Your point about the trillions of Dollars in “cash piles” – this is additional evidence of the overall fall in ROC globally…If cash could be invested more profitably than at zero plus zilch percent it would be… This is the real nub that in Capitalism 4.0 (or whatever you want to call it) is not regenerating capital at a rate that satisfies aspiration. That is why inequality is accelerating which people like you and me worry about. I am sorry if this is a shorter response than your comment deserves but please keep reading and commenting. Victor