February Mining Update

The market for medium and smaller miners – those developing and not yet producing – remains the worst anyone can remember. Yet unless you believe civilisation is about to collapse, the trend to decarbonise, which will require far more of certain necessary commodities than present plans imply will be available, will absolutely demand that they be found. And it is not the giant mining conglomerates who find them. It is the minnows, who the majors rely on to spend their own risky money, but who are being denied efforts to raise it.

Funding is there if lenders think commodities will be healthy, But at the moment they’re not – certainly if you factor in the general inflation which is said to be seriously increasing other mining costs. It may reflect local conditions and a specific project’s bad management, but the just announced 87% increase in Horizonte Minerals’ Araguaia Nickel project construction cost (even though already half-complete) will be a serious worry for all other would-be mining projects and their shareholders.

To compensate for those increased production costs, commodity prices will have had to rise substantially, yet the metals index which in the 2008 junior mining slump fell by 60% is down from its peak a year ago by ‘only’ 30 – badly distorted by nickel, down 40%, with copper down only 10%, having been down 30% meanwhile.

Those falls mostly reflect pessimism about the Chinese economy, which used to account for 50% of all copper usage, and is flooding the nickel market with projects it is funding in the Philippines.

Gold of course is about the only commodity showing strength (while lithium continues down) so what are the lessons for investors? Perhaps to concentrate for the moment on gold, and on projects already built and ready to produce. Among those are a few I’ve been recommending like Pan African Resources and Hummingbird Resources, and even KEFI Gold and copper.

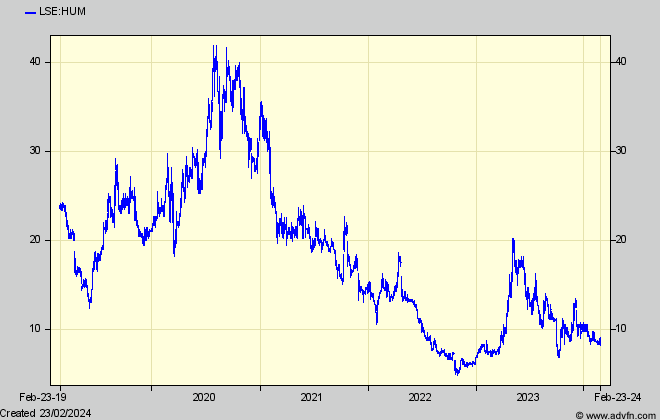

Hummingbird (HUM: market cap £68m @ 8.5p) is still bedevilled by the pessimists, despite recently reporting that “a strong FY-2024 outlook positions the Company for significant deleveraging and growth”.

It’s its new Kourossa mine (while the original Yanfolila keeps going) which will deliver the wherewithal to repay its HUM’s borrowings that underlies my recommendation for what would be a transformation in the company’s valuation. Currently, its ‘enterprise value’ (which is the key professional investors go by, rather than the ‘equity’ value which mostly influences private investors) is inflated by adding its debt to its equity market valuation, making it look expensive.

But the “material balance sheet deleveraging” (through Koroussa ramping up, so as to more than double HUM’s gold production)is promised will commence in Q1-

2024 – with scheduled debt repayments of c.US$77 million in the year, c.US$61 million in FY2025, and the remaining c.US$15 million by the end of FY-2026

But the pessimists are assuming that won’t happen, in the same way HUM missed its forecasts for Yanfolila last year. But those were mainly for reasons outside HUM’s control (weather, subcontractors having to be replaced) and while the usual mining pitfalls could also dent Kouroussa (already its ramp up was delayed for a month by a country-wide fuel shortage – now fixed) and would give the pessimists more ammunition, the sheer size of the contribution it can make is why the potential for transformation is so large and why I stand by my recommendation.

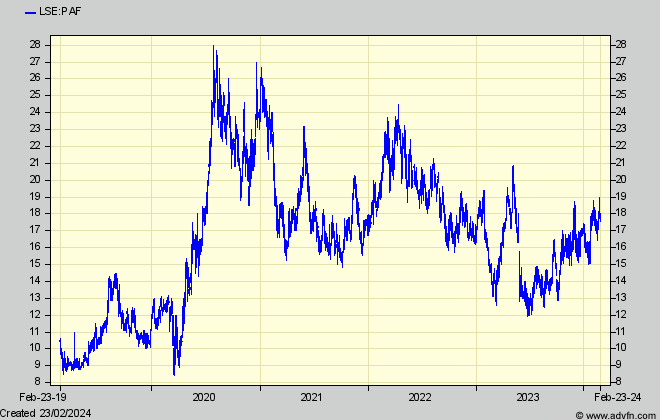

Pan African Resources (PAF: market cap £339m @17.7p) is another miner in the right commodity, who has already spent on new capacity and has recent problems hopefully behind it. Its existing gold projects have a relatively high mining cost (at $1,300/oz) which means that a rising gold price will gear up its profits more than for others with lower AISC’s, and in addition its newly acquired Mintails gold tailings project will come on stream at the end of this year, increasing full year gold production by 25%, at better margins.

Those positive were what was expected two years ago when I recommended the shares, only for strikes at PAF’s key Barberton Mine to decimate them – but when I said Hold On. Now, PAF is upbeat about progress even before Mintails starts contributing, so the shares are currently strong – but still cheap.

After more than a few years of false starts, KEFI (market cap £37m @ 0.75p) at last looks to be within sight of building its Tulu Kepi gold mine, having gained solid promises from all funding parties and met all conditions for the $320m needed. That is except for $20m still to be raised at the level of the project itself (ie not from Kefi shareholders but probably from Ethiopian locals).

Construction should start this Spring, and with more clarity on the complex funding structure, the company has updated the economics as will be seen by shareholders, as opposed to the picture published so far which was as presented to bank and other funders needed to get them on board. (I hope readers know that project economic numbers are always ‘as seen’ from the point of view of a particular participant at a particular date – and that, eg, the NPV will change as money is spent and earned and as time goes on)

Those economics look attractive now for shareholders – being a NPV for them at an 8% discount, of 3.4p per share from Tulu Kapi alone, neglecting KEFI’s other gold finds in Saudi Arabia. The only threat to that (unless production and costs don’t go as planned) is from the issue of more equity shares, which looks likely but not serious.

More easily understood than an NPV, and what will determine the share price once in production from mid 2026, is that is that total cash built up over Tulu Kepi’s 7-9 year life will be $800m, or an average of $62m pa for Kefi’s 70% of the project compared with its current $39m market cap. That is not what will be reported for the first few years however, when profits will bear substantial loan interest, but the underlying profit should reflected in a share price much better than now. By then also, Kefi’s two other exploration projects, in Saudi Arabia, which the co says will be almost on a par with Tulu Kepi and will soon produce preliminary feasibility studies, will themselves be much further on. So. all in all, although investors will have two years waiting to see if the plans are working, Kefi is one of the few shares that at the moment look likely to be out of the starting blocks once the current market malaise clears.

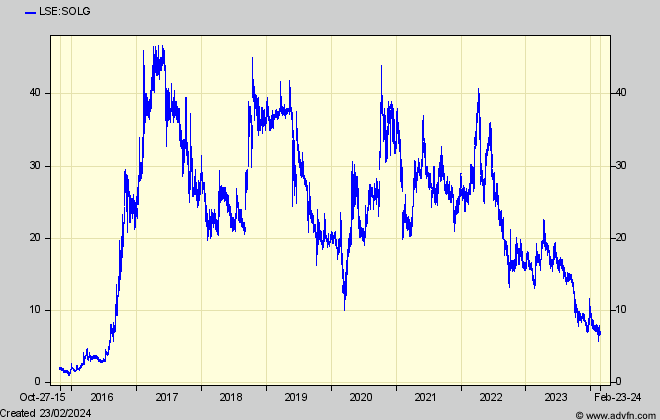

I haven’t mentioned Solgold – market cap £204m @ 6.8p – for some time. But its experience also provides a lesson right now for Greatland Gold, which is why it’s timely to update.

Although SOLG is in that dangerous category of miner with project not yet built, it has just published an up-to-date economic study for a drastically revised mining plan at its flagship Cascabel copper/gold project in Ecuador (which we can assume takes account of that frightening cost inflation) which looks so much more easily handled than previous ones, that investors are starting to take more interest. Especially because, as a result of a long recent history of disappointments and problems, Solgold’s valuation has sunk to a level that would have seemed unbelievable only 18 months ago.

Now, at 1/5th its then share price, Solgold’s £204m market cap compares with £117bn worth of gold and copper measured and indicated resources ‘in the ground’ at Cascabel alone – regardless of other promising exploration prospects. That is a value only 0.2% % of high quality resources, when in healthier mining markets valuations for most mining projects would be in the 1-2-3% ranges.

I first recommended Solgold here in March 2016 at around 3p, and made a healthy packet as I hope readers did – that was at first when the size of its find at Cascabel made it seem destined to be one of the largest in the decade. But then, despite BHP and Newcrest taking key stakes, things started to go pear-shaped – essentially because management did as well.

By about 2019, fears Cascabel would be too expensive to develop were confirmed by the first of a series of feasibility studies, which showed an initial cost of $2.5bn, and would be followed by $6.7m of discounted cash profit over an enormously long 55 year mine life subsequently (although most would have been earned in the first 15 years).

And although that would have delivered an annual rate of return of 25-26%, it was considered a bit too marginal for such a risky project in a risky-looking Ecuador, quite apart from the cost being too hefty for a small company like Solgold to manage.

Allied with that, a key issue was – as I started warning here – that then CEO and founder Nick Mather was following the wrong strategy to monetise his fast growing portfolio of other attractive looking finds. He wanted to create a monster mining conglomerate – whereby all would be kept within one financial group, whatever each project’s different needs and timetables would be for development funding. That meant that coming to shareholders to fund each project as it developed would produce a share price below what the furthest advanced would have attracted on its own.

It was that basic strategic mistake stemming from Mather’s ambition that has been playing out up to now, with a series of management clear-outs including Mather, and a share price too low to maintain spending on the 10-12 other exploration projects he was pursuing, and, more seriously, even to maintain development on Cascabel

Now, following a long needed merger with key Cascabel shareholder Cornerstone, the latter’s management has taken over, although hadn’t yet been able to lighten the gloom.

Since the 2019 feasibility study, Solg has been bending to shareholder demands for a more easily funded plan, if not for a sale of its various projects, so now it has come up with a new Cascabel study for a cut-down plan showing an initial capital cost of only $1.6bn, still (at a higher $1,750/oz gold price) showing a 24% rate of return, but over a mine life half the much-too-long 55 years of the previous plan. At what are fairly conservative copper and gold price assumptions, and with scope to expand production from other nearby resources, Cascabel looks a much more feasible proposition, with a far better chance that some bidder or funder will come along.

But the shares are still depressed – not only through uncertainty how any funding will affect value for shareholders, but also because Solg has spent most of its remaining cash on the new study, so that investors worry about another fund raise (which the company has said might have to be) to keep the company running.

What happens next I don’t know. But maybe things can’t go on like this? Even if funded now, it will take ten years before Cascabel is making the $450m annual cash profit the feasibility study estimates for the first 5 years in production, before doubling over the next five – at the conservative $1,750/oz gold price it assumes, and $3.85/lb for copper. The current $2,000 gold price would add nearly 20% to those economic returns.

But meanwhile could be the sale of one or more of the other projects (to help fund Cascabel – a step Mather was refusing to take) among which Porvenir in southern Equador has already found over 7Moz of gold equivalent (mostly in copper) – a substantial find in its own right

So what lesson for Greatland Gold and its 30% owned Havieron project? It has now been confirmed by Newmont that it will be divesting its 70% Havieron stake, which – with substantial cost to develop (that Newmont seemingly thinks not worthwhile) looks to be much too big a mouthful for GGP to swallow on its own. It means, like Cascabel’s effect on Solgold’s shares, that investors will worry about the effect on GGP’s share price of whatever large new partners might demand to come aboard and help fund Newmont’s 70% Havieron stake. Its why it’s still wise to stand back and watch GGP -instead of assuming that its large project means a large profit for its small shareholders.

Comments (0)