A Recovery And Copper Story For The Top Drawer

Jubilee Metals (LSE:JLP, JSE: ) 3bn shares at 7p = £212 m market cap.

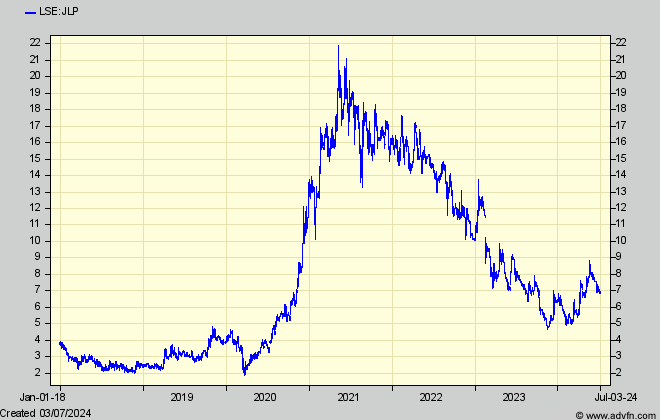

Jubilee Metals since 2018

After many years spending and positioning itself, Jubilee Metals (was Jubilee Platinum until 2017) looks like being on the cusp of fast growth – as it builds on its expanding PGM and Chrome recovery business in S Africa – although in the face of weak Platinum Group Metals prices – to create a hopefully faster-expanding and equally profitable copper recovery business in Zambia.

JLP’s share price history however reflects the long process of getting together the methods, plants, and resources to do so before benefiting from them. Having commenced 20 years ago with licences in the Bushveldt platinum fields, Jubilee concentrated on treatment and refining rather than mining, so that between 2015 and 2021 having branched also into chrome it saw rapid revenue and profits growth – only to run into Covid and a steep fall in PGM demand and prices. Peak profits of £43m and eps of 1.8p in 2021 slid to only £13m and 0.48p respectively in the year to June 2023, but are already beginning to turn around.

JLP is unique in the mining space – because it doesn’t actually do the expensive mining bit, but instead buys up some of the vast number of surface spoil heaps and ponds in Africa containing the waste from past mining which was not considered economic to treat and refine further to a saleable product – at a time when mining yielded much higher grades than today. As a consequence, grades useable by today’s methods were left behind in the waste. (Goldplat (LSE:GDP) is of course one such treater of tailings, but concentrating on gold and, much smaller, has experienced lumpy contracts producing lumpy profits)

Rather than for gold, Jubilee has been perfecting – for a wide variety of industrial metals and types of waste – the ‘benefication’ and refining techniques that recover saleable product, usually much more profitably (because the waste is a nuisance and can be acquired cheaply) than for a complete mining operation.

The shares’ recent behaviour shown on the chart however was in a period when Jubilee had first expanded into Zambia, through purchasing rights in 2018 to the extensive lead, zinc, vanadium, and copper waste left in surface tailings at the historic Kabwe mines, together with its associated Sable refinery. But while since 2018 Jubilee has spent nearly £200m (1/3rd of revenues) to acquire and upgrade facilities to refine copper and other metals, and to acquire more copper resources, towards the end of the period its previously highly profitable PGM recovery business in S Africa ran into much lower PGM prices.

That spending was met without borrowings, but from earnings and a necessary recourse to shareholders, who since 2022 have contributed over £50m – or 38% of total spending – and which capital raising, on top of the drastic fall in profits in S Africa after 2021, led inevitably to the sharp fall in the shares from their 21p peak.

Spending has been in both Zambia on copper, and in S Africa on expanding and upgrading Jubilee’s chrome recovery business there which has been replacing, more profitably, its original PGM operations, as well as installing power supplies to obviate the power cuts that have been plaguing African industry.

However, that substantial investment is only now tailing off and should soon begin to bear fruit, so investors might think there is every prospect of returning to those early 2021 share peaks – except for noting that shares in issue are now 2.3 times more numerous, meaning a 9p price today is the equivalent of 2021’s 21p, for the same market cap.

Obviously therefore at 7p the shares are already looking forward to a big chunk of any recovery. (A lesson, that inexperienced investors often don’t learn – to never trust ‘chartism’ when a company has been severely diluting its shares. Unfortunately, despite being asked, the share chart merchants have never got around to supplying the market cap charts that would be a better guide than share prices. Such a chart for Jubilee would squash that 2021 peak down to 9p)

However, the expectation and plan is that revenues and profits will recover from now on to considerably more than in 2021 – which is why a shareholder call in January at 5.5p was oversubscribed, and why soon after, the company broker WH Ireland for the first in a long time, published in February a very detailed research note, and why the company has just appointed RBC Capital as joint broker. Each has much to talk about, so the shares can expect to benefit from wider publicity once those brokers are convinced how quickly the spending benefits will come through.

Because, at the moment, they are proving to be slower than Ireland anticipated in February, where its forecast of a 27% revenue increase this year to June has been suspended after the interims to December showed ‘only’ 18.4% growth, casting doubt whether its forecast of doubled revenues by 2026 will be met.

That benefit is not yet showing through because copper production in Zambia (although not chrome in S Africa) has been held back recently while the plants are being upgraded or integrated. New plants are in the form of small ‘modules’, which can be operated more flexibly that a traditional bulk plant and lead to better efficiency, but vital components have been held up in transit from abroad leading to copper revenues which grew only slowly from £3m in 2020 to £17m last year when gross profit fell to only £5m gross profit compared with £7.7m in 2022.

However, in the latest 2024 half-year to December, copper gross profit in Zambia increased by 67% on a 23.5% increase in revenue so – except for a more recent hiatus in new module delivery in the half year just ended – the fast growth expected in Zambian copper looks to be already on the way.

Meanwhile growth has been coming from Jubilee’s PGM and chrome business in S Africa which still contributed 88% of 2023’s group revenues and has seen a 296% profit increase in the latest half-year on a further 46.5% revenue increase. As in Zambia, Jubilee has been upgrading and expanding its chrome recovery activities in S Africa, where it reckons to be the market leader and, as well as recovering chrome and PGM’s from waste, also offers toll processing for miners.

But it is in Zambian copper where Jubilee is most excited by prospects and has stated an ambition to expand annual production to 25,000 tonnes – over 7 times recent levels – for which deals have already secured more than enough raw material resources to be refined into copper cathodes via two new or upgraded plants. In addition is a new joint venture with AbuDhabi’s International Resource Holdings to treat higher grade mined ore rather than partly processed and lower grade waste.

One of the new plants, Roan, which is planned to contribute 1/3rd of that 25,000 tpy copper, is only now coming on line, having suffered from the delays mentioned in procuring some of the vital plant components. Similar delays upgrading the original Sable refinery at Kabwe which is slated to contribute 2/3rds of that capacity are currently worrying observers and causing brokers to go cautiously with forecasts, and naturally this is being reflected in the shares. While Broker WHI’s February research forecast ‘only’ 27% revenue increase this year, it turned out at half-way stage to be ‘only’ 18.4%. so that WHI has suspended its full year forecast, and will obviously be revising its February forecast of a 90% revenue increase over the 3 years to June 2026 and then eps of 1.3p.

On any normal rating that would not command much more than the current share price for a ‘mining’ operation in Africa (with its erratic politics, and complications translating results via often rapidly changing exchange rates) However, that would not include a premium for growth, while Ireland’s forecasts do not take account of what could be future increases in the copper price and the attraction to investors looking for exposure to it.

So it seems to me that, while I don’t expect a spectacular 2021 style recovery in the shares, their current hesitation before the pace of Jubilee’s expanding business becomes clearer offers an opportunity to tuck some away.

Comments (0)