Pershing Square Holdings re-positions its portfolio

After a couple of strong years the listed hedge fund Pershing Square Holdings (LON: PSH) has had a more modest six months with returns held back by the delayed investment in Universal Music.

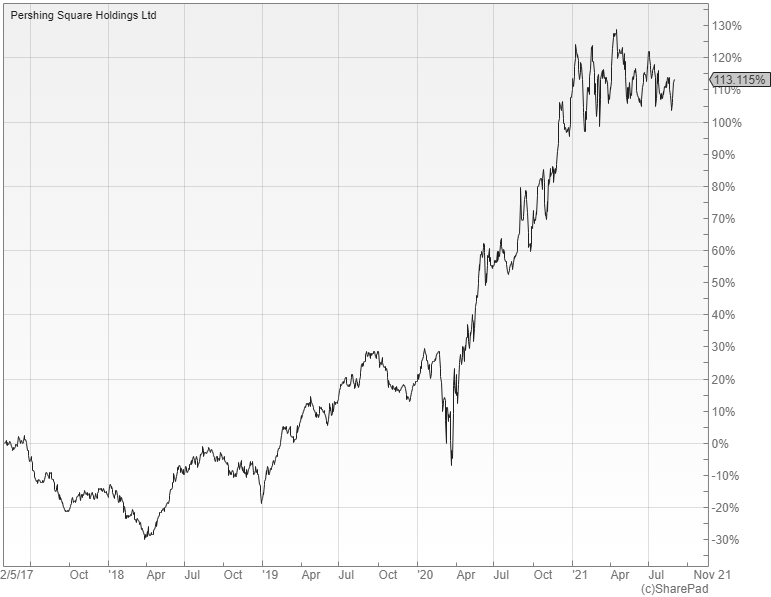

Bill Ackman’s £7bn hedge fund returned 7.3% in the half-year to the end of June, which was well behind the 15.2% achieved by its S&P 500 benchmark. I doubt that investors will be complaining too much though as it has had two exceptional years with gains of 58% in 2019 and 70% in 2020.

The main drag on performance was Pershing Square Tontine Holdings (PSTH), a special purpose acquisition company, or SPAC, that raised $4bn in its IPO. PSH along with other Pershing Square funds is committed to contributing extra cash when it does a deal and has exposure via sponsor warrants and forward purchase agreements that are marked to market.

Ackman attempted to use the SPAC to acquire around 10% of Universal Music, but regulatory concerns about the structure of the transaction prevented the deal from going ahead, a move which cost PSH 4.7% in the reporting period and almost seven percent year-to-date. The SPAC is currently looking for another company for its initial business combination and is also grappling with a contested lawsuit that alleges that it has been operating in the US as an illegal investment company.

Changes to the portfolio

Since the end of the reporting period PSH and otherPershing Square funds have bought 7.1% of Universal Music by more direct means and they also have the right to acquire a further 2.9% at the same price by September nine. Universal will become a public company by the end of the third quarter when Vivendi distributes 60% of the stock to its shareholders, at which point it will become PSH’s largest portfolio holding by a substantial margin.

Ackman believes that Universal is a high-quality business with a strong management team and strong balance sheet that is well-placed to benefit from the shift in favour of streaming services in the music industry. He is comfortable with the size of the position based on his view of its low probability of capital loss and the outlook for long-term growth.

The only other portfolio changes in the period were the sale of the position in Starbucks and the purchase of an initial investment in Domino’s Pizza, the number one pizza company in the world. Agilent Technologies was sold after the reporting date as it approached its estimated intrinsic value with the proceeds being put towards the investment in Universal.

A unique approach

Pershing Square holds meaningful stakes in nine US-listed stocks with the other key positions including: Lowe’s Companies, The Howard Hughes Corporation, Chipotle Mexican Grill and Hilton Worldwide, many of which have benefitted from the re-opening trade over the last year or so.

Ackman is also able to use derivatives to protect the portfolio and did so successfully during the Covid-inspired crash last March, with a further hedge currently in place to guard against the risk of rising interest rates due to higher inflation.

PSH is a unique vehicle and has an exceptional track record over the last two and half years, yet despite this the shares have tended to trade on a wide discount to NAV that currently stands at 27%. There is obviously a lot going on at the moment with the SPAC and the purchase of Universal, but Ackman has shown himself to be adept at adding value, although some may baulk at the high costs and the influence the manager wields via his large personal stake.

Comments (0)