Hard hats on and hunker down it’s all about to get a lot worse

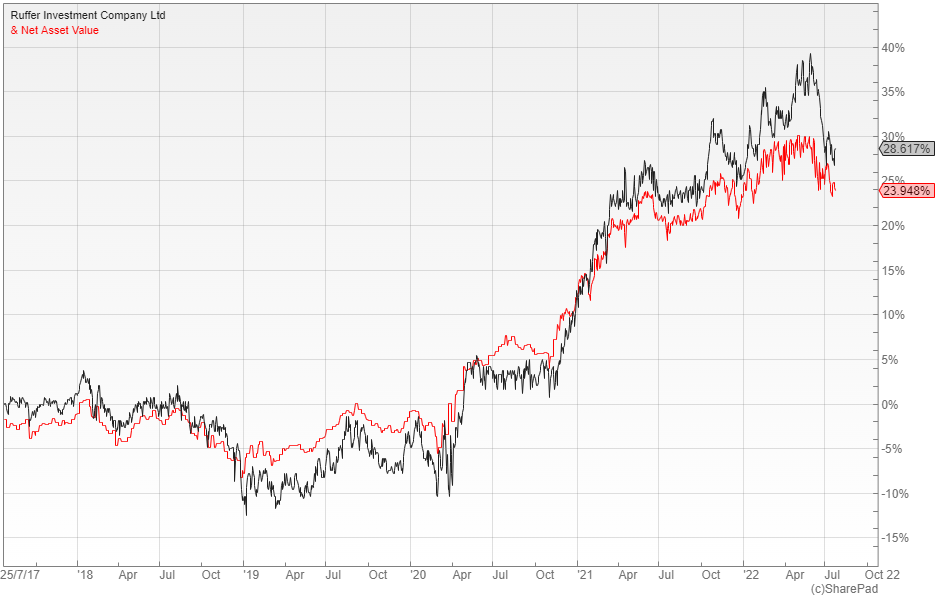

Ruffer (LON: RICA) is a defensive multi-asset investment trustthat aims to preserve and grow shareholder capital. It has just released its year-end review for the 12 months to the 30 June in which it reported a steady 5.6% share price total return, although it is the tenor of the investment manager’s outlook that is the most noteworthy feature.

In the latter part of the period they reduced the risk in the portfolio, moving into what they call ‘crouch mode’ for what they think will be a particularly dangerous environment in the second half of 2022. The changes included a reduction in the equity weighting to 25%, with hedges on top for good measure, which makes it the lowest allocation for Ruffer portfolios since 2003.

They also boosted the portfolio duration, as the recent rise in bond yields has increased its potential effectiveness as a hedge and rotated the gold exposure from equities to bullion. The upshot is that a full three-quarters of the fund is now invested in protective assets, namely: cash, short-dated bonds, index-linked bonds and gold, as well as illiquid strategies and options.

Grim outlook

In the long-term they are expecting a return to the sort of spasmodic bouts of inflation volatility that we saw after the Second World War and again in the 1970s. They think that we will endure an extended period of accelerating financial repression – where interest rates are held below the rate of inflation − forcing negative real returns upon savers.

It is a grim outlook for a staccato, stop-start world of higher inflation and faster economic growth. This will be driven by targeted government stimulus to tackle the big societal issues of the day such as inequality, climate change and the containment of the geopolitical aspirations of China and Russia.

The more immediate problem is the impossible tightrope walk that the central banks are trying to negotiate. If they tighten financial conditions too much to get inflation under control then unemployment will surge, the economy will tip into recession and asset markets will get crushed, but if they don’t tighten enough the risk is that inflation will get embedded into wages and we will end up with the dreaded wage-price spiral of previous inflationary episodes.

Hard hats on

Investors under the age of 60 have been conditioned to buy the dip as central bank easing has always been just around the corner, but a look further back in history shows that many bear markets start with a steep drop, followed by a more prolonged grind lower over a number of years. Ruffer think that this is where we are now as the political imperative is to bring down inflation, not to support asset prices as in previous market sell-offs.

They see the next few months as a period to hunker down and survive, given the extent of the uncertainty around the Ukraine war, central bank policy, inflation, corporate earnings and the consequences of rising interest rates. With all of this coming as the tide of easy money recedes, it is not a time to be taking too much risk.

Ruffer has a long track record of delivering steady returns to shareholders and I personally think that its allocation to illiquid strategies and options gives it more of a solid floor than its nearest rivals Personal Assets (LON: PNL) and Capital Gearing (LON: CGT). The company has experienced heavy demand in recent months and has issued a lot of new shares – the number of shares in issue have increased by more than 50% in the past year – to mop it up and keep the premium from getting out of control.

Comments (0)