FED’s Next Move… Negative Rates?

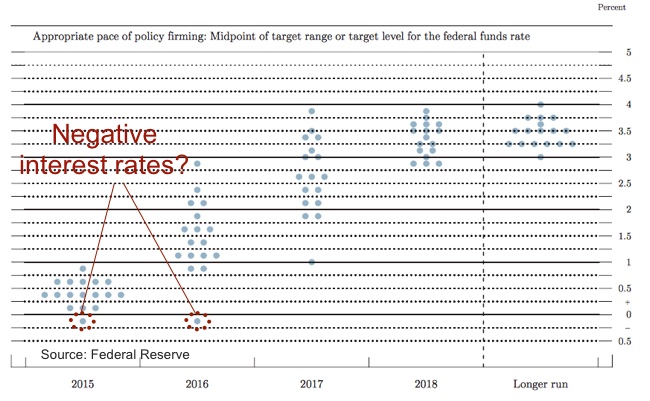

Is there anybody who still believes the FED will hike rates this year…? The next? With the latest developments in mind, I dare to say the FED may be closer to another round of QE or even to setting negative rates than to a rate hike. Yesterday’s FOMC meeting and policy announcement not only kept the current 0.00% – 0.25% rate bracket unchanged but also replaced the hawkish tone of the previous statement by a new dovish, blame-the-others statement. Negative rates were even considered, no matter how fiercely Janet Yellen may oppose them.

Since central bankers found the power of the “communication with the public” as a monetary policy tool, they have vigorously adopted it to massage future expectations to help achieve their goals. But such communication skills work well when the massaged expectations do materialise, otherwise the central bank would just lose credibility. Such has been the abuse of the tool that the FED is at the point of losing its credibility, as investors behold a world that is substantially different from the fantasy the FED depicts.

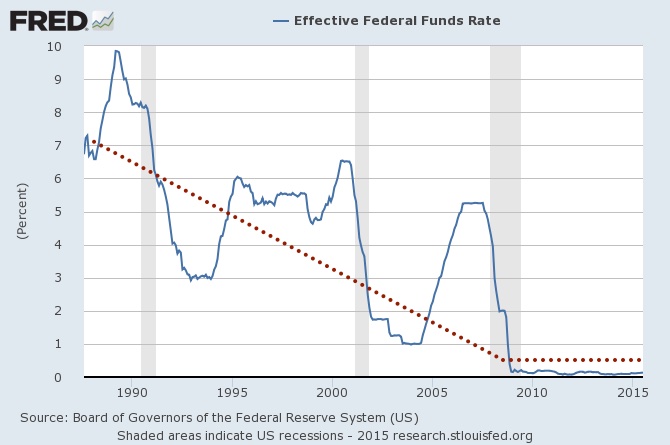

The last time the FED touched interest rates was 16th December 2008, when it cut its benchmark rate by 75bps in an attempt to contain the systemic damage the Lehman collapse could create. That was the 10th straight cut in a period of one year and three months, which trimmed the interest rate from 5.25% to 0.25%. In terms of rate hikes, we have to go back to June 2006, when the FED hiked its key rate from 5.00% to 5.25%. Almost ten years later and the FED wasn’t able to manage even the slightest rate increase of just 25bps.

Interestingly, yesterday’s statement foresees the key rate at 0.4%, 1.4% and 2.6% for 2015, 2016 and 2017 respectively. If raising rates by just 25bps is taking years of preparation and word massaging, I wonder how the FED plans to hike rates to average 2.6% in 2017. I would say the current predictions owe more to faith than to reason. The clock is ticking. For the predictions to materialise, the FED needs to move to 0.5% over the next meeting or to more than 0.5% in the following one. That is not going to happen because the FED would hit the economy hard, even if indirectly through the financial sector. That is the collateral damage that is created when the central bank puts the cart before the horses and tries to boost the real economy through an increase in the price of financial assets, which should otherwise just reflect the economy. Given the leverage involved, these assets usually disconnect from reality. At the first sign of smoke, which usually occurs when there is the slightest tightening in credit conditions, the bubble is pricked and a blood bath ensues.

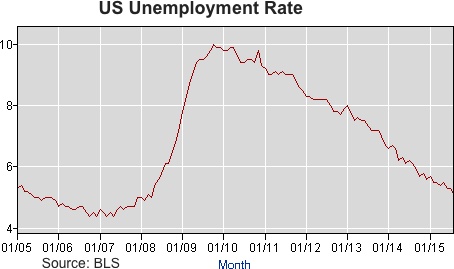

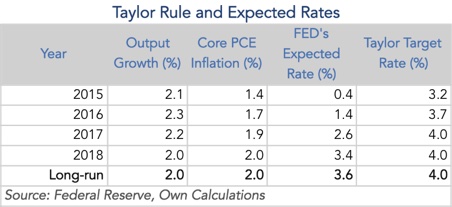

When Ben Bernanke was chairman of the FED, policy action was made dependant of domestic data (or at least believed to be that way). Bernanke promised to keep QE running until the unemployment rate decreased to a 6.5% level – a rules-based approach. At the same time, employment data, inflation pressures and economic projections have always been made pivotal in dictating the following steps the FED would take. But that worked as long as the FED was finding justification in the data to keep the status quo. That is no longer the case as the central bank predicts the US economy to grow 2.1% this year and slightly more over the next few years, which is above its long-run expected growth rate. That means the US economy is near its potential growth. In terms of jobs, the situation is similar to the GDP scenario. The FED predicts the unemployment rate will keep declining and hovering around 4.9%, which is also predicted to be closer to full employment. In terms of inflation, and taking the core PCE index (the favourite FED’s inflation gauge), predictions are for a rise of 1.4% in prices this year, 1.7% in the next and 1.9% in 2017. Under such scenario the Taylor rule would advocate an interest level between 3% and 4%.

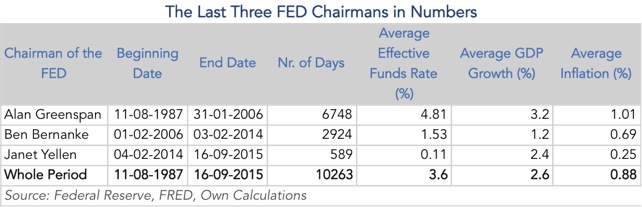

That comes as no surprise, as a level of 4% has always been interpreted as the target long-term interest rate, which corresponds to a 2% target inflation plus a 2% real rate of return. The current projections the FED makes is for a 3.6% rate, which is not far from that value. Additionally, if we compute the average effective funds rate since August 1987 when Alan Greenspan became chairman of the FED, the average rate is exactly 3.6%.

Why does the FED insist on keeping the interest rate near zero, when everything including its projections point to a much higher value? Because they know that as soon as they hike rates the massive bubble created in the financial market will be detonated creating shock waves through the real economy. The reason why this is going to happen is because monetary policy doesn’t create wealth in the long run, but just leads to price increases instead. Ben Bernanke would strongly disagree and asks in a defiant tone: Where are the price increases?

There are no price increases when you measure them with CPI and PCE measures. Look elsewhere in the financial market and you’ll find them, in triple digits. Shorter monetary intervention could have served to contain the crisis at the time of the Lehman collapse but the FED kept the policy unchanged for years without normalising it, and thus has been inflating asset prices and creating bigger problems, instead of allowing the economy to orderly get rid of the waste it created in the past. In the end, there should be no bewilderment when facing an increase in emerging market debt, an increase in the wealth gap in the US, and a lack of a vigorous global growth.

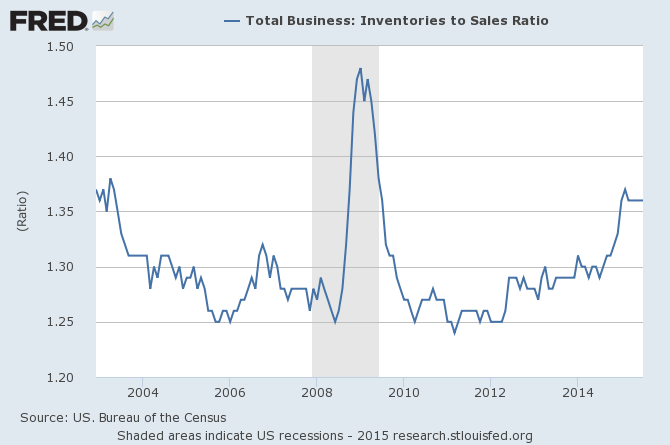

Low interest rates mean money is essentially free, and when money is free people do take actions lightly. Just try to trade the equity market with free money in a virtual portfolio. Then try the same but with real money. You’ll allocate money differently! The difference comes from the fact that it hurts losing money. Risk is only an issue when real money is involved. Transpose this idea to the current economic scenario and you’ll help to explain the erroneous investment decisions that tend to occur with near-zero interest rates. Every investment looks stunning! Projects that take a longer time to achieve results will attract more money than they would if rates were naturally set – that is, more capital goods than needed are produced. At a time when the economy is trying to get rid of excess capital goods, all the central bank attempts to do is to convince people to produce even more capital goods. That is nonsensical, as it kicks the problem into the future instead of addressing it in the present. And of course such investment doesn’t lead to sales but rather to an accumulation of unsold inventories.

When interest rates start rising again, most of these projects will shut down. If Instead the interest rate was set higher, the economy would have allocated more resources towards consumer goods, which would not only help the economy recover but also allow it to get rid of excess capacity.

But for the FED, all that matters is keeping the Dow Jones and the S&P 500 alive and up in the sky, so that there is an increasing probability the FED will keep rates at very low levels indefinitely. Now that the domestic economy is no longer a reason to hold fire, the FED is blaming the global economy. Interestingly, the FED, on one hand blames China as being the main reason for not hiking rates; but on the other hand retains the expectation that such a problem doesn’t change future inflation. The central bank has trapped itself inside a box it cannot open. I may be wrong but it seems to me that we won’t see any rate hike over the next few months if not a year (at least without being quickly reversed).

It seems strange that at a junction the world is waiting for the FED to move on towards normalising its policy, there is one policymaker who is considering a rate cut towards a negative value. In doing so, he is simply destabilising the markets even further.

So, once again asking the question: why is the market declining when the FED just did what investors were looking for?

While the interest rate affects the present value of the future cash flows of companies, there is one thing in the FED’s statement that directly affects the cash flows themselves – the massive downgrade the FED has made to its projections for the global economy. By not hiking rates and pointing to global uncertainties, the FED has just led investors to believe that global growth is set to decline, and with it, of course, corporate cash flows. On the one hand you get the same discount rate but ont he other you get trimmed cash flows…

Janet Yellen is safe for another month. The ball is now in the hands of the BoE and the ECB… the market will need them… the BoE to stay quiet… and Super Mario to become the hero again, this time by expanding the asset purchase programme.

Comments (0)