Attractive entry point for the Baker Steel Resources Trust

A delay to the sale of its largest holding has resulted in a significant derating of Baker Steel’s shares, which could represent a decent, long-term buying opportunity.

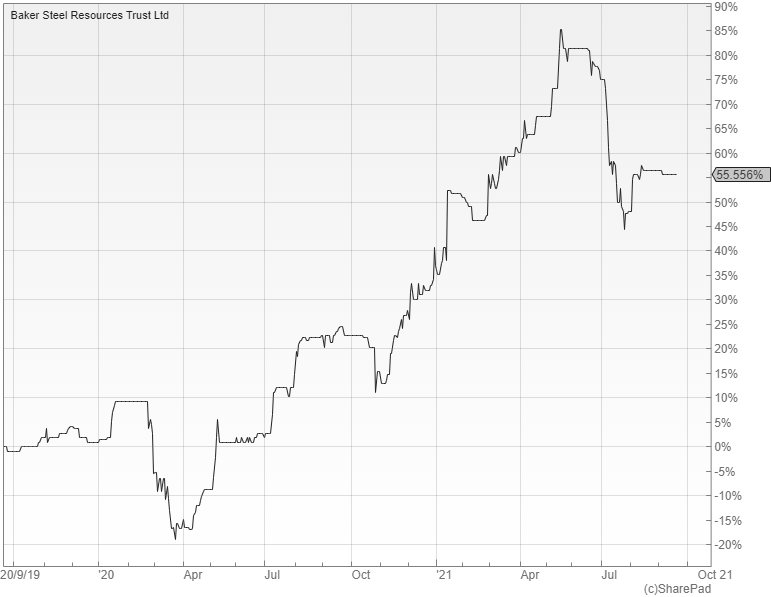

The £103m Baker Steel Resources (LON: BSRT) is a unique investment trust that offers exposure to a focused portfolio of natural-resource projects via stakes in unlisted companies and specialist listed opportunities. Its shares have fallen back from a recent high of a pound to 84 pence and currently trade at a discount to net asset value (NAV) of 13% after a frustrating half year for its biggest position, Bilboes Gold.

Bilboes Gold is a private listed company that owns a gold mine in Zimbabwe and is the fund’s largest holding, at 19.4% of net assets. It reached outline terms for a partial sale of the business to a large gold producer, but was unable to come to a final agreement.

The sale was adversely affected by travel restrictions imposed because of the pandemic, with potential buyers unable to visit the site and meet with management in person. Despite the setback, Baker Steel believes that it remains an attractive project and is confident that its value can be realised, with the company currently investigating a potential IPO as the best way forward.

Slowdown after an impressive 2020

The company’s mining shares did well during the economic recovery from the pandemic in 2020, with Baker Steel’s NAV rising 29.3% in the year, but its performance since then has been more muted. An increase of 2.7% in the first six months of 2021 was followed by a decline in July and August of 3.2%, due to a material fall in two of its smaller positions.

Baker Steel’s second-largest holding accounting for 16% of net assets, Futura Resources, has also been held back. The output from its coking coal mines in Australia is used to supply the steel industry and it was hit hard by the ban on imports from China in late 2020. However, the unofficial embargo has since been removed, with coal prices more than doubling as a result.

This is the problem with having a highly focused portfolio where 12 positions account for most of the assets, as the returns are almost entirely dependent on the fate of the major projects. There are however a number of positive developments on the horizon that could make the current dip an attractive entry point.

Reasons to be cheerful

Three of Baker Steel’s key investments are currently nearing a listing; the first is Tungsten West. The company owns a tungsten mine in Devon that accounts for 15.7% of net assets and is planning an IPO on AIM for October.

Then there is First Tin Limited. It represents 5.2% of net assets and is anticipating an IPO in the first half of next year, due in part to the increasing demand for tin as a key resource in the shift to electrification. A similar timescale is also envisaged for the Norwegian copper project, Nussir ASA, which makes up another 3.9% of the assets.

IPOs like these provide price discovery and a route towards liquidity, but as a major shareholder, Baker Steel would probably have to enter into lock-up agreements for a certain period to ensure an orderly market in the new shares. However you look at it though, these sorts of mining companies appear to be undervalued in absolute and relative terms compared to the broader stock market.

Comments (0)