John’s Mining Journal: featuring Asiamet Resources and Horizonte Minerals

Veteran mining analyst John Cornford reviews some of the more interesting plays in the junior mining sector…

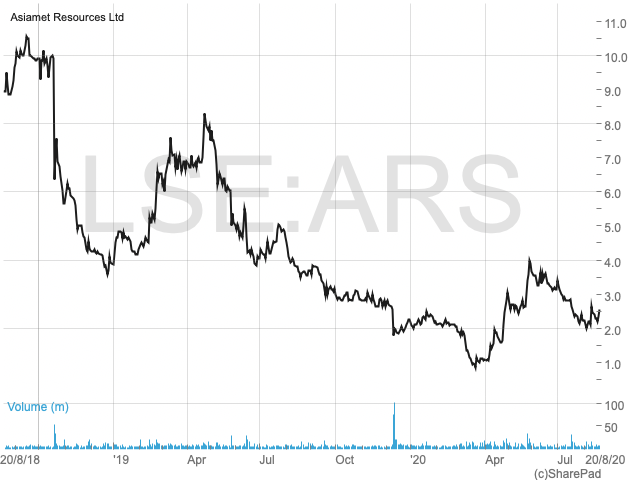

Like Kefi Gold and Copper (LON:KEFI) (formerly KEFI Minerals) Asiamet Resources (LON:ARS) (formerly Kalimantan Gold – except that it is mostly copper) has a mining project that has been in waiting for some time, with fits and starts that have tested the patience of investors. At present the shares are in the doldrums and present an opportunity for an uptick at some stage – perhaps soon. But while it has longer term prospects, I don’t think they are as good, yet, as Kefi’s.

I’ve written about ARS in the past, when I was sceptical about the value of the feasibility study then awaited for its BKM (Beruang Kanan Main) copper project in what used to be Borneo and is now the Kalimantan province of Indonesia. Expectations for its value provoked a spike in the shares until, having touched 12p in March 2018, they collapsed when the study showed a lower rate of profit than investors had anticipated.

A later update at bankable level in June 2019 was only slightly better, showing an 8% NPV of only $133m against a $192m initial capital cost, even at the $7,400/tonne assumed copper price (vs $6,000/tonne now, and a recent low of $5,000/tonne). The IRR came in at a not very spectacular 19.5%.

With cash costs of $4,000/tonne, today’s gross profit margin at $6,000/tonne would be 40% less than in that study, and net margin even lower, while the NPV might almost vanish.

Nevertheless, everything has a price – particularly a large project – and even a nil NPV would be worth pursuing by a government willing to finance it, for the copper exports it would produce and the employment created. So with a copper shortage forecast in the longer term, and with work meanwhile to identify opportunities to ‘enhance’ BKM’s value and to extend the mine life through promising exploration nearby, Asiamet has found possible partners to help bring BKM into production.

In August 2019 it signed an MOU (memorandum of understanding) with China Non-Ferrous Metals Corp to source the engineering to build the mine, and in March this year placed new shares with a Singapore based conglomerate, Aeturnum Energy, to give it a 19.9% stake in ARS and to start a due diligence process aimed at Aeturnum making a strategic investment in BKM at project level.

So, investors are waiting to see what price Aeturnum will pay for a stake, or even to buy the whole project or put forward funds to build it. But Aeturnum’s enquiries are progressing more slowly than hoped due to Covid-19 restrictions, and it has become embroiled in a court case in Singapore concerning deals over a valuable oil consignment in which it is only one part of a chain, so is not necessarily at risk except from delays. But it has, recently, confirmed that it still intends to make an offer.

But the resulting jitters have kept ARS’ shares depressed, despite Tony Manini, ARS’s CEO, reassuring only recently that as far as he knows Aeturnum is still committed. Further reassurance stems from the directors’ recent decision to opt for payment of their 2019 fees in shares (4.85m of them) at 2.46p, instead of cash as is their entitlement.

So, if they are right (or lucky) there is the scope for a quick bounce in the shares if Aeturnum comes up trumps. Even if it doesn’t, all would not be lost because ARS has other copper prospects in the same area of Kalimantan, such as BKZ, BKS (BK ‘South’) etc, along with its larger Beutong copper and gold project in Sumatra. The latter is not as highly developed as BKM, but has promise of becoming even larger, and with 2.4 million tonnes of copper and 2Moz of gold already drilled, it is currently some 20% the size of Solgold’s Alpala project (which is the largest new prospect globally in the last ten years).

(Interested investors can see a recent webcast by Tony Manini at https://asiametresources.com/media/)

It is good to see that Horizonte Minerals (LON:HZM) has almost come up with most of the remaining project finance to construct its flagship Araguaia ferro-nickel project in Brazil – the first of two – the second aimed at supplying the different and more promising EV battery market.

In my suggestion to track HZM in a detailed review last October, I said not to chase the shares (at their then 4.7p) but to track for the longer term – which would have given investors looking to a recovery in nickel demand an opportunity when the Covid panic forced the shares down, momentarily, to 1.7p in March.

The spike to 5p just before my review had followed Orion Finance kick-starting funding for the project, with an initial $25m streaming deal, and I said the market was waiting next for the rest of the $445m needed to start production, when some thought it might be worth 10p per share (although I disagreed).

That funding has now almost arrived in the form of a banking consortium promising to raise a $325m loan, targeted to be finalised by the end of this year. That event has spurred the shares back up to 4.9p, posing the question whether the momentum is now strong enough to punch through the previous 5p trading range top.

That probably depends on how the nickel market performs. Currently around $14,500/tonne, the price seems to be on a recovery trend from a Covid-induced $11,500 low in March, so could continue strong to the $16,133/tonne which HZM expects will apply when Araguaia starts up. At that price, the 8% NPV would be around $600m – seven times the current market cap – and would more than double when the second stage Vermelho battery nickel project starts later.

Subject to obtaining the loan, however, HZM will almost certainly raise new equity, which is when we will see whether the market will pay up to the mooted 10p. So my advice meanwhile is to track and to buy only if the shares drift a bit, but otherwise to wait and see.

It’s also good to see how Scotgold (AIM:SGZ) has been responding to the gold price and to its re-starting preliminary work at its Scottish gold mine. While it must be good for UK investors to have exposure to gold on their doorstep, it should be noted that the gold price in sterling is different to its performance (as is always stated) in dollars. The latter’s weakness recently against world currencies has been one reason (though not the only one) for gold’s strength. That doesn’t dent SGZ’s attractions, however.

Comments (0)