While the US Federal Reserve and the ECB have been busily adopting counter-cyclical measures aimed at stabilising economic growth and price increases, commercial banks have been at the other extreme, always frustrating such measures and acting pro-cyclically. The Fractional Reserve system that allows for faster credit creation than the economy can absorb is the main reason why we have been experiencing frequent financial turmoil, in a repeated pattern that persists over time. When the central bank fails to retain control over the money supply, monetary policy doesn’t work – at least not in the intended direction/strength and/or in the nation’s interests. Hence, why the Federal Reserve had to stretch the monetary base by $3 trillion just to reap mild economic results. And that also explains why the previous interest rate hikes have not been enough to prevent the credit boom that led the global economy towards collapse.

{kind=link}

But while the ECB and the Federal Reserve prefer to be in a never-ending power struggle with commercial banks regarding money creation, it seems that Iceland is on the verge of taking the power back to the central bank. That’s right! Iceland is heading towards the end of the Fractional Reserve system, willing to turn its commercial banks into mere financial intermediaries no longer able to create credit out of thin air and will.

Heading From Crisis To Crisis

The idea that unbounded credit expansion can lead to financial crises imparting profound economic consequences is not new, nor is the idea that banks have an active role in the whole process. Charles Kindleberger (in his “Manias, Panics, and Crashes: A History of Financial Crises”) and Hyman Minsky (in several works) have both alerted readers to the role of the credit provided by banks and to the role of the development of new financial instruments in the genesis of a full-blown crisis. Banks and other institutions have always found ways of improving the efficiency of the stock of money and thus often circumvent the attempt by central banks to limit and control the growth of the money supply. Minsky explains that too much credit expansion almost always precedes a financial crisis.

It all starts with an initial displacement or a positive shock. The consequence is a quick increase in optimism, which spreads across lenders, borrowers, investors, businesses, and households. The boost in sentiment leads to a distortion in the perception of risk and seduces people towards bearing more risk than before. Commercial banks then expand lending to the economy, acting pro-cyclically and undermining any counter-cyclical measures adopted by the central bank. The increase in credit leads to further increases in optimism and the system becomes self-fulfilling, until it evolves into a mania, a panic, or a crash.

Iceland Studies Alternative Monetary Systems

With the works of Kindleberger and Minsky in mind, and in particular the fresh memory of a deep financial trouble, the Icelandic Prime Minister commissioned a study on the future role that should be attributed to the Central Bank of Iceland and how the monetary system should be designed to prevent financial chaos. The study, conducted by Frosti Sigurjonsson (a lawmaker from the ruling centrist progress party) and concluded last month, identifies the same vicious cycle Minsky always alluded to and goes the extra mile of providing advice on how the current Fractional Reserve system can be converted into a Sovereign Money system under which the central bank recovers its full power regarding money creation and commercial banks are prevented from expanding credit beyond the central bank defined targets. While certainly applauded by the Austrian School of Economics, such an idea will most likely be shouted down by mainstream ‘neo-Keynesian’ economists such as Paul Krugman and severely opposed by a battalion of commercial banks that make their living out of eternal credit displacement.

Sigurjonsson’s report shows that since 1875 Iceland faced over 20 instances of financial crises with 6 serious multiple financial crises. A serious crisis occurs every 15 years on average. While being mandated with independence – in order to be able to control money creation, inflation, and contribute towards overall economic stability – the Central Bank of Iceland has been unable to prevent the unhealthy risk-taking that almost always leads to a financial collapse, to major economic disruptions, and to costly state interventions. The reason behind this is relatively straightforward. The central bank targets the short-term interest rates and expects to influence bank lending through the effects this intervention generates on the yield curve. But, ultimately, money creation will depend on the commercial banks’ willingness to lend, as they have the power to decide how much they want to lend to the economy in spite of any initial incentive generated by the central bank.

Thus, the central bank creates the incentives for banks to lend and banks lend funds up to the limits imposed by the reserve requirements. That is not correct! In fact, not only do banks have the power to expand credit; they can also extend it without limit. Just take the Eurosystem as an example. Banks are required to keep 1% of clients’ deposits as legal reserves. This should mean that for each €100 deposited, they must keep €1 aside, right? Not exactly. The ECB keeps an unlimited lending facility that allows banks to tap any necessary funds to cover any shortfall they may experience in their legal reserve account. So, if banks find it fruitful they can lend €200 with just €1. Then, at the end of the reserve period they borrow the €1 that is missing to comply with the requirement. Needless to say, such system only works as long as there is a government assurance on deposits, otherwise the system would be severely exposed to bank runs, as it is technically bankrupt from the beginning.

In cases where the reserve requirement and other capital requirements are binding, bankers possess the engineering tricks to create derivatives to circumvent the system and expand credit beyond limits, as Lehman Brothers, Fannie Mae, Freddy Mac, help remind us. So, we can safely say that commercial banks are pretty much unbounded when it comes to credit creation.

Commercial banks are certainly influenced by the short-term interest rates the central bank attempts to manipulate, but they still retain almost the full power regarding money creation. That explains a lot. Why has the Federal Reserve expanded its balance sheet by trillions of dollars? Why has the Federal Reserve just accomplished mild results in terms of boosting investment and growth?

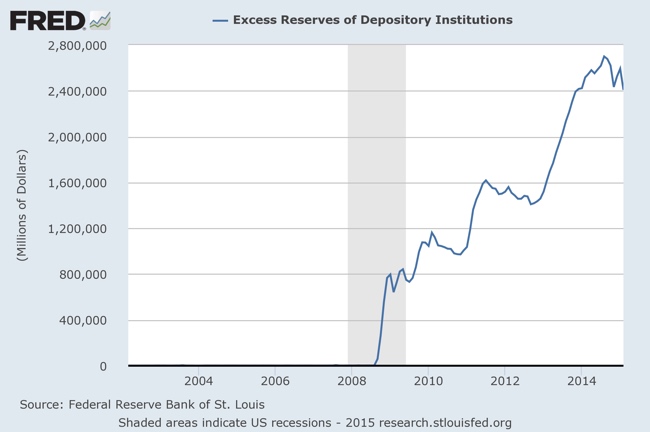

The answer is plain and simple: because banks haven’t used the money to lend. Instead of lending the extra money, banks used it to repair their balance sheets and to deposit any excess reserves back at the central bank. To convince you to borrow from me, I am willing to lend you £100 at almost zero interest. But, as you don’t see any opportunities to use the money, you take the money but ask me to keep £95 in my wallet. Not happy with it, I am willing to lend you another £100 at an interest rate that is even closer to zero. Again, you take it but ask me to keep £98 in my wallet…and so on. That is exactly what central banks have been trying to do. They’re desperate for banks to pick up the funds and lend to the economy, but that is not happening because central banks no longer have any control over the money supply. The above situation is very well depicted in the chart below. There has been an astounding increase in bank excess reserves over the last few years, which coincides with the massive expansion of the Federal Reserve monetary base.

{kind=link}

At some point, if bankers change their minds regarding lending, the US may face hyperinflation. Again that will happen at commercial banks’ will, not the central banks’.

Under such a Fractional Reserve system, instead of acting in the nation’s interests, the central bank is a mere tool for commercial banks to use at their discretion, as they ultimately retain the power to create the money they desire. As banks often act pro-cyclically, they tend to expand credit when there is economic expansion and to contract credit when the economy is in recession. But those actions contrast with the central bank interventions that are in exactly the opposite direction and therefore undermine the effectiveness of monetary policy. In the end, central banks fail to achieve their objectives and financial crises are more likely. The result often sees the state taking on big losses – as most of these banks are too big to fail – or a spiral into full-blown economic crisis, which in either case represents an overall loss to society.

With such evidence, it easily follows that the Fractional Reserve system is rotten and must be replaced by something different, even if against the will of many. That is the reason why Sigurjonsson proposes a so-called Sovereign Money system as a full alternative to the Fractional Reserve system currently in place. The idea is to take the power from commercial banks and hand it to the central bank. Under such a system, there is a clear line drawn between the power to create money (attributed to a central bank) and the power to allocate money (attributed to the banks). But then banks would be financial intermediaries, which I guess they don’t want to be.