QE’s benefits are fading… quickly

Risk and volatility are increasing rapidly, as investors reassess whether more easing is really a good thing or just the confirmation of a global central banking failure. US markets are way overvalued due to the trillions the FED injected into the market over so many years. At a time industrial production and employment data are coming in much softer than expected, and the risks of a bear market are increasing. While currently not under discussion, a potential recession in the US cannot be discarded, in particular if the deterioration in economic data continues to gather pace. For now, all we have is a small market correction, but if the weakness continues, it may turn into a bear market. The FED was very unfortunate in its timing to normalise policy and its credibility may be affected if it pulls back from policy normalisation just three months after starting it. An opportunity to raise rates was missed long ago and now the FED is arrested in a turbulent financial market environment. But they should have known from the very beginning that the risk of boosting asset prices through monetary policy is that of the real economy undershooting the rally in financial markets. The gap must be filled at some point.

When an economy enters recession, consumer and business confidence both decrease very quickly. Weakening sentiment leads to an increase of risk awareness: consumers start saving more and businesses cut back on investments and on hiring, as they watch their inventories accumulate rather quickly. As a result of this, unemployment increases and output decreases. To a certain extent, the adjustment is needed for the economy to get rid of past excesses. But these adjustments usually involve a downward spiral where lower consumption leads to lower investment, higher unemployment and lower output, and then lower output also leads to lower disposable income and lower consumption again. Some circuit breakers are needed to help rebuild confidence.

In 2007-2009, the FED needed to act to prevent the liquidity squeeze from affecting the real economy. After all, it’s the central bank’s role to provide adequate levels of liquidity. But, the FED did much more than provide liquidity as necessary; it flooded the market with unneeded liquidity that flew in the direction of the equity market and other risky investments. In my view, that should have been the role of the central government. At a time when a liquidity squeeze was contained by the central bank and sentiment was battered down, the positive externalities that could come with fiscal policy would be at a maximum. The government could have acted as a circuit breaker to help restore confidence. I am not advocating massive government intervention but just pointing out that, if there ever was a time to do something…

In a time of deep trouble, the US government acted more like an additional burden on the economy than as a Good Samaritan. With the help of the FED and the global hegemony of the dollar, the US Treasury was able to finance a rising debt pile at ever lower rates for decades. But when government fiscal policy was needed the most, Congress was playing fiscal cliff and the economy had to rely on a central bank purchasing assets en masse to create financial wealth where real wealth didn’t exist.

One should credit the FED for having boosted the US economy in the short term. At the peak of the crisis unemployment was hovering at 10% but it then started to decline, eventually hitting the current 4.8% level. Nevertheless I believe it also created severe global imbalances. The dollar declined and boosted commodity prices for years; low interest rates led to massive capital flows in the direction of emerging markets; central banks in emerging markets could keep record low rates while companies were able to issue large amounts of debt. Now that the time for normalisation has come, all of this has been put into reverse: the dollar has been appreciating; commodities have crashed; emerging markets have experienced large outflows that have led to large currency devaluations; and corporations face tougher conditions to repay their dollar-issued debt.

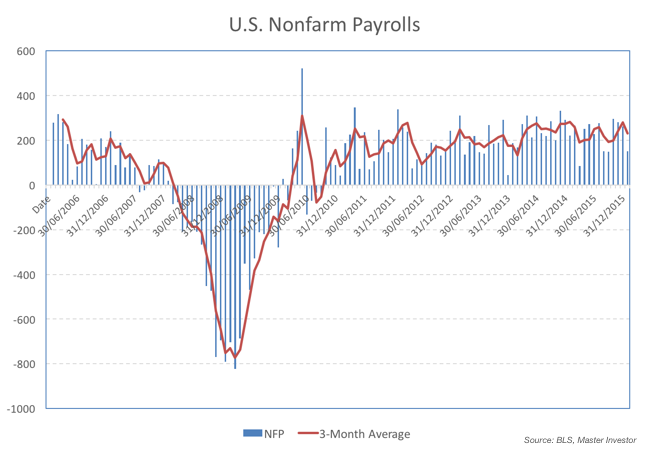

The turmoil generated by a hike in interest rates in the US and a rising dollar may quickly spread to the real economy. For now, we can say that economic data has been showing a significant improvement since the height of the crisis. After all, the unemployment rate is now at 4.8% as the economy is adding more than 200k jobs per month. But it is undeniable that for the last few months the data have been softer than anticipated. For now there is no material reason for concern, but if the “softer” leads to “weaker” data, a recession may arise, at a time when interest rates are already at rock bottom.

The data released on Friday showed that nonfarm payrolls increased 151k in January. The report also showed a decrease in the unemployment rate from 4.9% to 4.8%. Despite being a positive report, the numbers fell short of expectations.

The report also showed an increase of 12 cents in hourly earnings, suggesting that disposable income may be increasing, which may help boost consumption. However, at the same time, productivity is decreasing, making wage growth unsustainable.

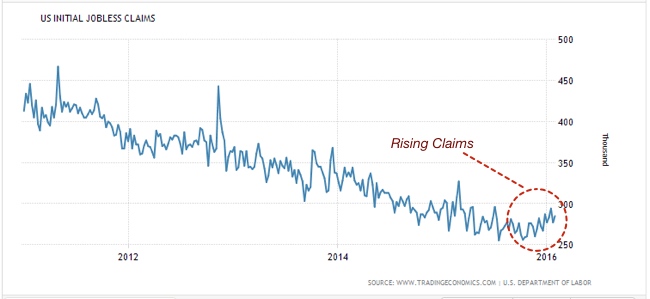

The “softness” is confirmed by the initial jobless claims data (which is released every week). While still below 300k (a level often seen as the point at which unemployment starts rising), the numbers have been increasing for the last few months and are now near six-month highs.

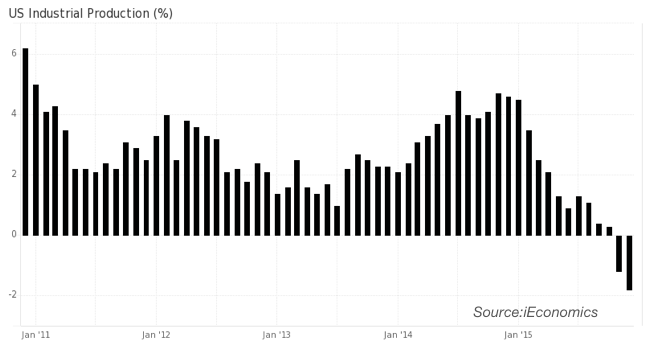

At the same time, job creation seems to be losing strength, and industrial production is also softening. In fact, the latest two releases point to a decrease in industrial production. These numbers can’t be taken lightly, because industrial production is a leading indicator for the US economy. Softness can turn into weakness later in the year.

Investors have been reacting positively to negative economic news and negatively to positive data. While such a reaction doesn’t make much sense, that’s the result of fostering a market which is dependent on central bank action. Every time the data is softer than anticipated, investors take it as increasing the odds of the FED postponing the next rate hike. By now many are already betting the FED won’t hike rates for the entire year, which is good news for equity prices. But one can also think about all this in a different way. If at the first sign of policy normalisation, economic data is already becoming softer, isn’t that a clear sign that QE is just a short-term solution? Isn’t that a sign that QE is a partial failure?

The FED is arrested by the equity market and will very likely avoid touching its key rate over its next policy meeting in March. I believe the recent weakness in equities is here to stay for some time. The process of rate normalisation will be kicked to the future and the world is nearer to negative interest rates than it is to any kind of normalisation. With many already discussing a cash ban as a solution for the zero lower bound restriction, it seems that gold is likely to shine once again. Investing in gold is a great hedge for the turmoil ahead.

Comments (0)