In 2008 Warren Buffet made a big bet against hedge funds. He claimed that an investor would be better off following a passive investment strategy by dumping his savings into a low cost index tracker than by handing them to a hedge fund that would actively manage the money for an expensive “two and twenty” fee. Seven years later it seems very unlikely that hedge funds still have any chance of collectively proving Buffet wrong.

There are at least two main reasons why an investor is willing to hand his savings to a hedge fund instead of building his own portfolio: (1) a diversified portfolio requires investing in so many equities that it is prohibitively expensive to do so; and (2) even if one could build such a portfolio, the stock picking ability a fund manager usually has can make a whole lot of difference in the correct allocation. Nowadays, we could say that the problem depicted in (1) is solved, as there are many passively managed ETFs (as well as other trackers) that mirror the performance of broad indexes like the S&P 500 that allow for an investment at very low fees. Regarding the stock picking abilities referred in (2), these are a specific characteristic of actively managed funds and then still a reason for an investor to pay for the services of hedge funds (or other active funds).

But, for (2) to be valid, Warren Buffet should lose his bet, otherwise the stock picking ability is not making a difference and thus an investor shouldn’t pay for it as he can still build a diversified portfolio on the cheap.

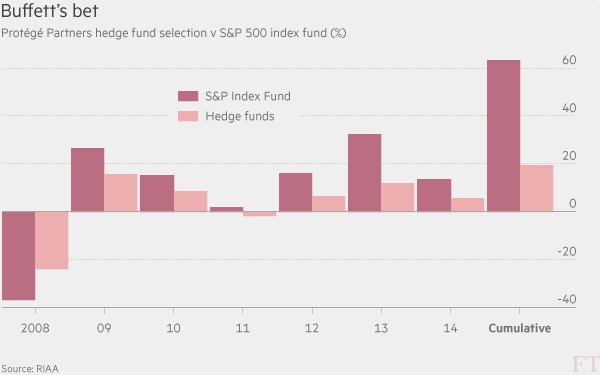

According to data provided by the FT, the S&P index fund that represents the passive management side backed by Buffet is significantly outpacing the performance of an index of hedge funds built by Protégé Partners to mirror the active management side opposed by Buffet. In the period between 2008 and 2014, the S&P index tracker accumulated a gain of 63.5% while the hedge fund tracker edged higher by just 19.6%, which is less than one-third of the passive performance. If this comparison is representative of the differences between the passive and active management industries, then one would say that hedge funds are expected to experience massive redemptions as there is no remaining reason one would pay the huge fees involved in active management.

{kind=link}

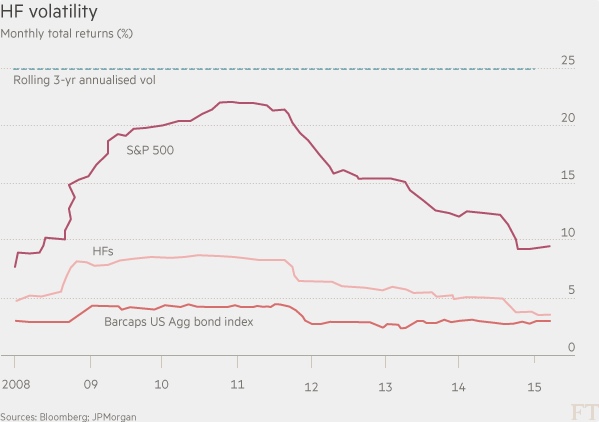

But, of course, hedge funds claim such a comparison isn’t fair because the risk involved in the S&P 500 is higher and thus explains the higher returns. In a recent report JP Morgan shows that average hedge fund volatility has been decreasing over the last five years and is now more similar to the volatility experienced in bond markets than in equity markets. The main explanation lies with the demand side for hedge funds, they believe. Institutional investors like pension funds are no longer able to even cover inflation expectations with long-term bond investments and thus look at hedge funds as an alternative to bonds. This presses hedge funds to adopt a more conservative style and explains the decrease in volatility.

{kind=link}

That explanation fits well with the data but just tackles the consequences of reality and not the reality itself. I hardly believe in hedge funds becoming bond-like investments! The decrease in volatility is a consequence of market intervention and not of a change in investment style.

Extreme monetary policy has extreme consequences in the market, with one of them being a decrease in volatility. Another is a decrease in the dispersion of returns. When interest rates decrease, equity and bond valuations rise. When the Fed buys assets, equities and bonds rise. When both actions are taken together and complemented with other tools tailored at managing market downside risks, asset prices move in one direction and with the same strength as if all assets were the same. The equity market is in a six-year bull run, having experienced just minor glitches. As a consequence, volatility could only decrease as depicted in the above chart. The S&P 500 has seen its volatility fall from a peak near 22% in 2010 to a low of almost 9% today. Every time volatility showed signs of life, some Federal Reserve Bank President came to the rescue with reassurances about the extension of the expansionary monetary policy. Monetary policy then drove down volatility in the markets, with both the decrease in equity volatility and in hedge fund volatility being a consequence of it. In other words, monetary policy has been erasing almost all risks, driving down volatility and dispersion of returns, and pushing investors out of the safer bond market in the direction of whatever they can find. With a market-wide decrease in volatility, every asset class seems safer than before and thus more “bond-like”. Hedge funds are no exception.

With equity dispersions being as low as they have been during the last few years, there is no fund management service that is worth paying for. No dispersion means that it doesn’t matter which stock one picks, as any one is a winner. Thus picking abilities are worth nothing. That explains most of the underperformance hedge funds have been showing. They just can’t beat the market by picking individual stocks and they either incur higher idiosyncratic risk or higher transaction costs than passive management. At the same time, rather than being a consequence of a change in their risk profile, the lower volatility experienced by hedge funds is part of a global movement. This coincidence is attracting money from desperate pension funds.

But ignoring the real risk profiles of hedge funds is a huge mistake that may put pension funds in danger. Long-term value comes from opposing a sentimental-driven market, something hedge funds no longer do, as 2007-2009 is proof of, with more than 90% of funds having been caught off guard at a time when most indicators were pointing to over-valuation and over-optimism. Let’s wait for the next bubble to burst and then talk again about that new bond-like style hedge funds have acquired…