Would Warren Buffett Buy These Small Caps?

As seen in the lastest issue of Master Investor Magazine

Warren Buffet is considered to be a great man for many reasons. For a start, the words of wisdom in his famous Berkshire Hathaway shareholder letters are so influential that they are widely quoted amongst the investment industry. For example, while working on the Master Investor magazine stand at last month’s annual conference I managed to catch three company presentations and all contained a quote by Buffett.

He also has the great characteristics of modesty (he’s still living in the same three-bed house in Omaha he bought over fifty years ago), philanthropy (having pledged over $30 billion worth of Berkshire Hathaway shares to the Bill & Melinda Gates Foundation) and self-criticism (admitting, “…I’ve made some dumb purchases”).

But at the bottom line, Buffett is considered such a legend amongst investors because of his track record of delivering consistent market beating returns over a career spanning more than fifty years.

How good is Buffett at investing?

As the chart below shows, the book value of Buffett’s investment vehicle Berkshire Hathaway grew at a compound annual rate (CAGR) of 19.2% between 1965 and 2015, equating to a total return over the period of 798,981%. Unsurprisingly, Buffett consistently beats the wider market as well – the S&P 500 with dividends included has only returned a CAGR of 9.7% since 1965. Notably, the firm has seen a fall in book value in only two individual years since 1965 – these, excusably, being during the tech collapse of 2001 and during the global financial crisis of 2008. In both years the falls were substantially lower than those seen in the S&P 500.

But this does not tell the full story. Buffett’s underlying performance has actually been much better.

As Berkshire Hathaway’s recent shareholder letters explain, the firm’s “intrinsic” book value far exceeds its accounting book value mentioned in the calculations above. This is due to a change in strategy during the 1990s, when Berkshire moved from owning partial stakes in companies to owning businesses outright. This resulted in stricter accounting rules being applied to the balance sheet valuation, whereby the value of losers is written down but winners are not revalued upwards. With there having been many more winners than losers, the underlying intrinsic value of the balance sheet is therefore much larger than its reported accounting book value.

This is reflected in the company’s share price having risen at a CAGR of 20.8% since 1965 (or a total return of 1,598,284%), well ahead of book value as investors realise the inherent value in the business. It is also reflected in Berkshire saying it is willing to buy back its own stock should it trade as low as 120% of book value.

Buffett tends to focus his investments on large US focussed companies.

However, his investment concepts can still be applied to UK small caps. The main concept he focuses on is the idea of an “economic moat”. This refers to when a company has a number of qualities which give it an economic advantage over its rivals over the long term. These can include a number of things such as strong brands, network effects, low operating costs/economies of scale and strong patents/intellectual property. Companies with such characteristics often have a high return on capital/equity (Buffett looks for 12% and above), strong cashflow and create consistent shareholder value.

It is no easy task to find firms with wide economic moats at the smaller end of the market given that small companies will find it harder to generate substantial scale benefits. But in this analysis I think I may have identified two companies which Buffett might just consider investing in.

NICHOLS

Warren Buffett is known for his love of Cherry Coke. But to put a bit more fizz into his returns he might want to try adding another well known soft drink to his portfolio.

Warren Buffett is known for his love of Cherry Coke. But to put a bit more fizz into his returns he might want to try adding another well known soft drink to his portfolio.

Nichols (NICL), one of the best small cap performers of the past decade, is a UK based seller of still and carbonated (fizzy) soft drinks. Its own economic moat comes via a strong portfolio of branded products, some of which have been around for over 100 years.

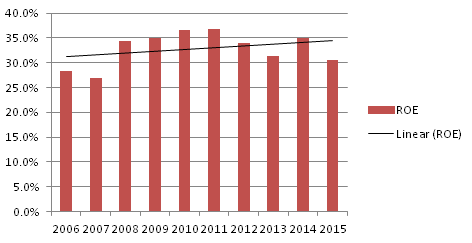

Although the company’s products are arguably not quite as well known around the globe as those owned by Coca Cola et al, it does have a solid market presence in the UK as well as a large presence in a number of countries around the world. It also delivers superb returns on equity which have averaged c.33% in the past 10 years – well above Buffett’s minimum criteria of 12%.

The moat is further strengthened by strong and stable margins which have been driven by operating efficiencies as the company has grown in size. Notably, Nichols’ operating margins are actually higher than Coca Cola’s (25% vs 20% in 2015).

Nichols historic return on equity

Nichols’ flagship brand is fruit based drink Vimto, which was first created in Manchester in 1908 by inventor John Nichols. Others core brands include Levi Roots, Feel Good, Sunkist and Panda, all of which are sold in the UK, the company’s core market which contributed 77.5% of revenues in the last financial year. Nichols also has a long history of growth in international markets. Its first overseas shipment was to Guyana in 1919 and now the company exports to over 70 countries worldwide, with key markets being in the Middle East and Africa.

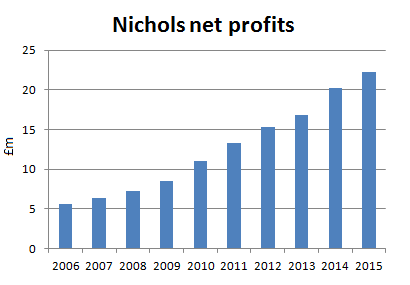

Nichols 10 year net profit growth

Further fizz in 2015

Nichols posted compound annual growth (CAGR) in net profits of 16.4% between 2006 and 2015 (chart above), with last year being another good one for the company. Revenue growth in 2015 was relatively flat at £109.3 million, with UK sales falling by 0.3%, offset by a 1.5% rise in international sales. But notably, reflecting the firm’s “moat” like characteristics, the UK sales performance was ahead of the wider soft drinks market, which according to industry analysts Neilsen fell by 0.6%. At the bottom line, pre-tax profits grew by a more pronounced 9% to £28 million mainly as the gross margin increased from 46% to 48.5%.

Another highlight of the year came in the form of two acquisitions. In March the company bought a 49% stake in The Noisy Drinks Company, and subsequently (in January) purchased the rest of the business. Noisy Drinks, a £6.6 million revenue company, specialises in frozen/slush drinks, selling the Starslush and Slurp brands to a client list including Merlin Entertainments and Compass Catering. Then in July 2015 Nichols acquired the Feel Good brand, an established range of premium still and sparkling juice drinks containing no added sugar and 100% natural ingredients. This deal may be important, for reasons discussed below.

A subsequent statement at the AGM in April revealed that trading in the year to date was in line with expectations, with the recent acquisitions of Noisy Drinks and Feel Good having an incremental impact.

Shares worth a pop?

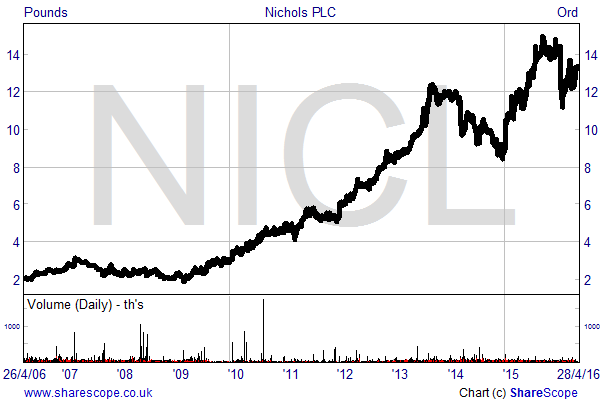

Over the past ten years Nichols shares have delivered capital growth of 547% (that’s a Buffett-esque CAGR of 20.5%) along with consistent dividend distributions. At the current price of 1,326p the company is capitalised at £490 million and at the time of writing is the 26th largest on AIM.

Despite announcing in January this year that trading was in line with expectations for 2015, the shares lost 22% of their value in little under two weeks. Then in March a subsequent recovery was set back by the announcement by the UK government of a so called “sugar” tax, which is to be implemented in 2018. Nichols looks to have plenty of time to address this, especially given that it already has a large portfolio of sugar free products – boosted by the acquisition of Feel Good.

In spite of this medium-term threat there still looks to be plenty of room for growth for Nichols. Its UK revenues of £84.8 million in the last financial year only give it a c.1.1% share of the £7.6 billion UK soft drinks market, with an even larger opportunity coming from the burgeoning international operations.

As is the case with most companies with solid economic moats, Nichols shares are not cheap, currently trading on a multiple of 20 times forecast earnings for 2016. Nevertheless, this looks to be a price worth paying given the firm’s track record. Dividend growth has also been consistent over the years, with 2015’s payment of 25.6p per share being up by 14.3% and representing a yield of 1.93% at the current share price. There is also the bonus of £35.4 million of net cash on the balance sheet which can be used to invest in further growth or to increase distributions to shareholders.

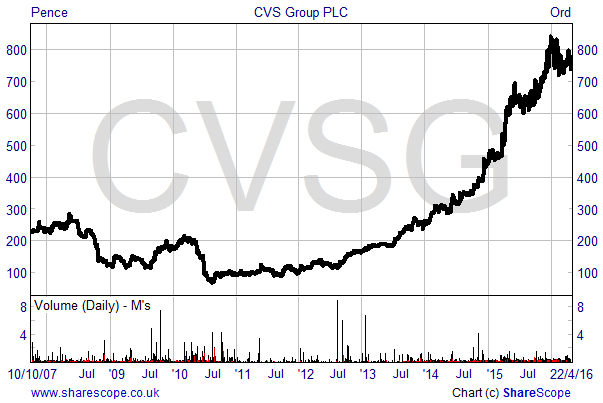

CVS GROUP

I could not find any evidence that Warren Buffett owns a pet during the research for this article. But if he does he will be well aware of how expensive it is to take them to the vets.

One of the leading vet owners in the UK is CVS Group (CSVG). The company was founded in 1999 in order to acquire and operate established local veterinary practices in the UK with a reputation for high quality service. Since listing in AIM in October 2007 the company, backed by significant debt funding, has increased its portfolio from 128 surgeries to 333 by the end of the last financial period in December last year. The firm’s relatively large market share provides it with an economic moat due to its significant buying power.

The veterinary practices are the core of the business, making up around 90% of current revenues. These mainly focus on the companion or small animals market (cats, dogs, hamsters etc.) and CVS estimates that it has a c. 12% share of this market. The equine and larger animal markets, of which the firm has a negligible market share, are also catered for.

Within the division, and providing a further barrier to entry for competitors, is the firm’s pet loyalty scheme, Healthy Pet Club. For a monthly fee of around £10 this provides members with a range of discounts and benefits and most importantly for CVS a crucial source of customer data – similar to Tesco’s Clubcard scheme which helped the supermarket giant build its own economic moat. Membership as at 31st December 2015 was c. 238,000 and contributed 12.6% of the division’s income in the last six month period.

The practice division also runs a referrals business which provides high value specialist services both to its own and third party practices. A referral is typically made when access to specialist knowledge or advanced equipment (such as CT scanning or key-hole surgery) is required.

The practices are supported by a number of other related operations, which give the company an integrated internal structure and the potential for significantly improving margins.

For starters there is the Laboratory division, which provides diagnostic services and in-practice laboratory analysers to its own practices as well as third party surgeries. The laboratories also supply in-house analysers and reagents to CVS’s own practices (thus boosting margins) and third parties. Then there is the Crematoria, or ”pet cemetery” business which operates six locations around the country where owners can cremate, bury and create a lasting memorial to their pets. Finally, Animed Direct is the company’s online dispensary business, which sells prescription drugs, non-prescription drugs, pet food and other animal related products.

Supporting all these businesses is the central administration function which provides finance, IT, HR and property functions, and supports economies of scale as the group grows in size.

CVS Group end customers

Growing the kitty

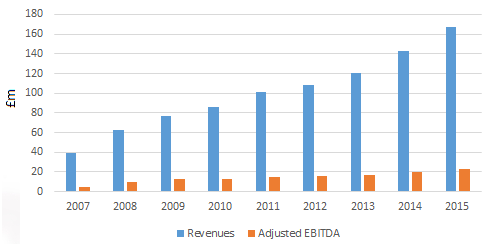

CVS’s rapid business expansion delivered revenue growth at a CAGR of 20% between 2007 and 2015, with adjusted EBITDA growing at a CAGR of 20.8%. I believe that adjusted EBITDA, which strips out amortisation and depreciation costs, is a better reflection of performance than statutory profits given large amortisation costs associated with the acquisitions. This is especially so given that EBITDA more closely matches the company’s net operational cashflow – the true measure of business performance.

CVS revenue and EBITA growth since IPO

For the six months to December 2015 further growth was seen, with revenues of £100.7 million up by 23% and surpassing the nine figure mark at the interim stage for the first time. Acquisitions were the main driver of growth but like-for-like sales were also up by a steady 3%. Adjusted pre-profits were up by 18% at £11.2 million.

Notably, the six month period was the most intensive in terms of acquisitions in the company’s history, seeing the purchase of 42 surgeries, two crematoria, the Vetshare buying group and the VETisco instrumentation sales business. As a result net debt rose from £46.2 million to £84.8 million by the period end. In November CVS entered into a new bank facility agreement which provides total borrowing facilities of £115 million, due for repayment in November 2021.

A purr-fect investment?

Warren Buffet would likely be pleased with CVS’s share price performance, it having delivered a CAGR of 16.2% since IPO in October 2007. My calculation of return on capital employed (adjusted net profits divided by equity + debt) of 16.4% last year would also meet his requirements.

At the current 739.5p the company is capitalised at £444 million. Like Nichols, the shares are not cheap as the market rates the company’s quality highly. The current PE multiple for forecast current year (to June) earnings is 23.5 times. CVS also pays a dividend, 3p per share in the last financial year. But with this representing a yield of only 0.4% I think the cash would be much better spent on reducing debt.

The large borrowings are one of the primary risks here, although I note that the position looks comfortable at present. Interest payments were covered 17.7 times by adjusted operating profits in the last financial year, leaving the company plenty of room for further deals to be done, and even to absorb any interest rate rises.

Comments (0)